General Discussion

Related: Editorials & Other Articles, Issue Forums, Alliance Forums, Region ForumsGenerally, young women's health insurance subsidizes the care of older men and women

if you don't want to pay for their maternity care, I suggest you prepare yourself for a big rate increase.

because the law is not going to allow excluding their maternity care, that is, unless it's changed to allow you to have a policy without maternity care, then they will be able to buy a policy that doesn't cover people with preexisting heart conditions or precancers.

if you think that's going to save you money, you are dreaming.

it will cost you.

believe me, if you are allowed to not contribute to young women's maternity care and you are a middle aged or older person --if you get your way, you are going to suffer as a result.

it's shooting yourself in the foot, and you don't even realize it.

i'm not young anymore but i read the writing on the wall.

YOUNG people who buy insurance make insurance cheaper for those older than them.

if you want to start cherrypicking which healthcare of the younger set you want to cover, i'd suggest you look at yourself and do the math of who on average is depending upon whom to pay for their care.

then look in the mirror.

this is why i see all our healthcare needs, male, female, young, old, middle aged as something we should all want to participate in covering --it's financially the best way for all of us, in the short run and in the long run.

anything less either puts us all at greater risk or makes individual coverage more, either now, or later in our lives.

we're all in this together. anyone saying they don't want to pay for maternity coverage because they can't have a baby --they are saying we aren't in this together, they are saying, cover my problem, don't cover that young woman's.

that kind of talk should be responded to for what it is.

= new reply since forum marked as read

Highlight:

NoneDon't highlight anything

5 newestHighlight 5 most recent replies

= new reply since forum marked as read

Highlight:

NoneDon't highlight anything

5 newestHighlight 5 most recent replies

daleanime

(17,796 posts)Arugula Latte

(50,566 posts)And people who specifically target and single out maternity care while ignoring all other health conditions/scenarios that could just as well pointed to are assholes, IMO.

CreekDog

(46,192 posts)pointing to some condition one doesn't have and saying they want no part of covering that --that is wrong on every level.

nomorenomore08

(13,324 posts)

Starry Messenger

(32,342 posts)joeglow3

(6,228 posts)CreekDog

(46,192 posts)...the person who thinks they don't need it.

i've been pretty clear on that.

joeglow3

(6,228 posts)You are saying if we allow people to opt out of maternity care, which is some thing many people will NEVER need (i.e. males, women past menopause & sterile women), we have to let people opt out of EVERYTHING, which mostly includes items that ANYONE can get (even if it the chance is remote for certain groups - i.e. young people).

I am not arguing that we should allow people to opt out of maternity care. It saddens me that these types of forced coverage would most likely have doomed the bill had people had full visibility to it prior to passing it. It is a necessary cost we need to shoulder to make insurance affordable for all.

I just pointed out the flawed logic you were using.

pnwmom

(108,973 posts)and there is no logical reason to deny women coverage for conditions related to pregnancy -- for which some people have a genetic susceptibility and which requires medical care -- and yet to retain it for other genetically related diseases.

In other words, under the ACA no one is barred from coverage or charged more because of their genes or their medical history. Even people with XX chromosomes, who have a tendency to grow cells inside one of their organs, will not be charged anymore than people their age with cancer -- who also have cells growing inside their organs.

joeglow3

(6,228 posts)Either that or you have convinced yourself an illogical point is actually a good one. Either way, you cannot be reasoned with.

pnwmom

(108,973 posts)I'll explain it to you again very simply.

Either we're charging based on genes and preexisting conditions, or we're not.

Since a person's genes or preexisting conditions will no longer affect their premiums, then half the population will not be charged more than the other half simply because they carry the XX chromosome.

Is that an argument you can follow or is it too difficult for you?

The National Women's Legal Center has shown that women have been paying $1 billion more a year in health insurance premiums for the same coverage men get -- even though maternity benefits are almost always excluded. IOW, maternity benefits, since they are excluded, cannot account for the much higher premiums women are charged. And neither can anything else. These higher premiums cannot be justified by actuarial statistics, because they vary widely among regions and across different companies.

If actuarial reasons explained all the higher premiums charged to women, then you would expect to see some consistency across regions and across insurance companies.

National Women’s Law Center

http://www.nwlc.org/sites/default/files/pdfs/nwlc_2012_turningtofairness_report.pdf

The practice of gender rating is rampant in the individual market.

• The vast majority of insurance companies charge women significantly more than men, even with maternity coverage excluded.

• To assess the prevalence of gender rating among popular plans in the individual health insurance market, NWLC examined gender rating among best-selling plans on eHealthInsurance.com.

As shown in Table 1, the Center found that in the capital cities of states that permit gender rating, 92% of best-selling plans charge 40-year-old women more than 40-year- old men for identical coverage. Gender rating is highly prevalent across and within states. In 31 states, all of the best-selling plans engage in this unfair practice. Moreover, of the best-selling plans that gender rate in 2012, only 3% include maternity coverage in the individual health insurance policy. Therefore, overall, maternity coverage does not account for the extra amount that women must pay.

• Based on an average of currently advertised premiums and the most recent data on the number of women

in the individual health insurance market, the practice of gender rating costs women approximately $1 billion in a year.7

There are approximately 7.5 million women who purchase health insurance in the individual market.8 Every month, women who live in states that allow gender rating are made to pay higher premiums than men for the same coverage. Over time, this additional cost adds up. When average currently advertised premium prices are applied to the number of women who purchase individual insurance coverage, NWLC calculates that aggregately, women spend approximately $1 billion more for health coverage annually than they would if they were men, not counting any additional costs women must pay because of the exclusion of maternity benefits.

• Such wide variations in the ‘premium gender gap’ exist, both within and across states, that any actuarial justification is highly questionable.

NWLC found substantial differences in rates charged among comparable plans across the country. To do so, the Center selected plans with a similar set of features (i.e., similar cost-sharing and deductibles) that did not include maternity coverage and calculated the difference in premiums—or the ‘premium gender gap’—charged to women and men at ages 25, 40, and 55. As shown in Table 2, there are wide variations in the premium gaps charged to women and men for health plans with similar features, both within states and across the country. For example, one plan examined in Arkansas charges 25-year- old women 81% more than men for coverage while a similar plan in the same state only charges women 10% more for coverage than men.

• NWLC found that significant differences in the premium gender gap also exist across insurance companies. For example, one insurance company examined charges 40-year-old women an average of 20% more than men for the same coverage while another company charges women an average of 50% more than men for the same coverage.9

•

• Such wide variations in plans with very similar features suggest that it is not merely actuarial considerations driving the price differences.

•

greendog

(3,127 posts)Stork bring you? I can't think of anyone who never benefited from maternity care.

joeglow3

(6,228 posts)Nice try, though.

CreekDog

(46,192 posts)good luck with that.

advocating not covering people with health care is a lot worse than saying something mean.

it's life or death.

advocating against maternity coverage makes DU suck.

and it makes America suck too.

congratulations. you know what that makes people think of you?

think about it.

joeglow3

(6,228 posts)I advocated FOR covering people. I just pointed out the comparison was flawed.

lumberjack_jeff

(33,224 posts)

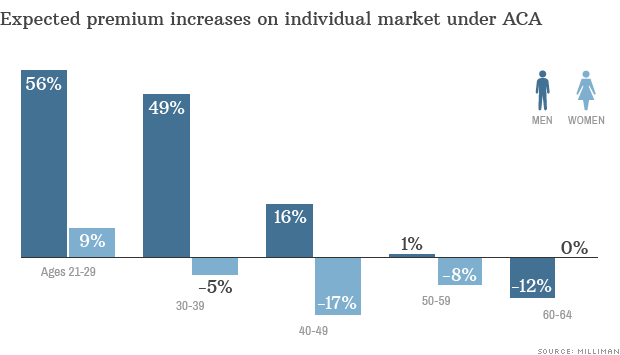

Yes, young people will pay more than older people but it's young men who are doing all the subsidizing.

pnwmom

(108,973 posts)(assuming your source is accurate) may merely prove that women have been subsidizing men up till now.

Demo_Chris

(6,234 posts)The reason that their rates are going down while young men's rates are going up is that young men are being tapped to help pay for maternity coverage.

Personally, I think this is fine. Not because it is logically incontrovertible on its own, but because I think it necessary to ensure that women have complete control over their sexual and reproductive choices.

pnwmom

(108,973 posts)Last edited Tue Nov 19, 2013, 07:23 AM - Edit history (1)

because only 12% of individual policies covered maternity care.

And women were hit with a double whammy. They were charged more for their policies EVEN THOUGH these policies excluded maternity and other care.

http://www.nwlc.org/resource/women-and-health-care-law-united-states

Women face unfair and discriminatory insurance practices, such as being denied coverage or paying more for health insurance than men. At the same time, individual market health plans often exclude coverage for services that only women need like maternity care. In most states, women are routinely denied coverage because of pre-existing conditions such as having had a C-section, breast or cervical cancer, or receiving medical treatment for domestic or sexual violence.

SNIP

Women who are able to buy health insurance on the individual market often have to pay more than men for the same coverage, a practice known as gender rating. 92% of plans practice gender rating.

SNIP

Starting in 2014, plans can no longer deny coverage to adults with pre-existing conditions. This means women will no longer be treated as a pre-existing condition and be denied insurance coverage for a history of pregnancy; having had a C-section; being a survivor of breast, or cervical cancer; or having received medical treatment for domestic or sexual violence.

National Women’s Law Center

http://www.nwlc.org/sites/default/files/pdfs/nwlc_2012_turningtofairness_report.pdf

The practice of gender rating is rampant in the individual market.

• The vast majority of insurance companies charge women significantly more than men, even with maternity coverage excluded.

• To assess the prevalence of gender rating among popular plans in the individual health insurance market, NWLC examined gender rating among best-selling plans on eHealthInsurance.com.

As shown in Table 1, the Center found that in the capital cities of states that permit gender rating, 92% of best-selling plans charge 40-year-old women more than 40-year- old men for identical coverage. Gender rating is highly prevalent across and within states. In 31 states, all of the best-selling plans engage in this unfair practice. Moreover, of the best-selling plans that gender rate in 2012, only 3% include maternity coverage in the individual health insurance policy. Therefore, overall, maternity coverage does not account for the extra amount that women must pay.

Demo_Chris

(6,234 posts)It is safe to assume they were charged more because they tended to use it more -- much in the way smokers are treated today, or young drivers when they get vehicle insurance, or someone on the Florida coast looking to cover their beach house.

There is no reason to assign malice when math provides the answer.

pnwmom

(108,973 posts)Last edited Tue Nov 19, 2013, 08:01 AM - Edit history (1)

If actuarial reasons explained all the higher premiums charged to women, then you would expect to see some consistency across regions and across insurance companies; instead there is marked variation.

Women were probably charged much more simply because the insurers COULD charge more.

So math does not provide the answer, according to this analysis from the National Women's Law Center.

FYI, women were being charged more than men even though only 3% of individual policies covered maternity care.

National Women’s Law Center

http://www.nwlc.org/sites/default/files/pdfs/nwlc_2012_turningtofairness_report.pdf

The practice of gender rating is rampant in the individual market.

• The vast majority of insurance companies charge women significantly more than men, even with maternity coverage excluded.

• To assess the prevalence of gender rating among popular plans in the individual health insurance market, NWLC examined gender rating among best-selling plans on eHealthInsurance.com.

As shown in Table 1, the Center found that in the capital cities of states that permit gender rating, 92% of best-selling plans charge 40-year-old women more than 40-year- old men for identical coverage. Gender rating is highly prevalent across and within states. In 31 states, all of the best-selling plans engage in this unfair practice. Moreover, of the best-selling plans that gender rate in 2012, only 3% include maternity coverage in the individual health insurance policy. Therefore, overall, maternity coverage does not account for the extra amount that women must pay.

• Based on an average of currently advertised premiums and the most recent data on the number of women

in the individual health insurance market, the practice of gender rating costs women approximately $1 billion in a year.7

There are approximately 7.5 million women who purchase health insurance in the individual market.8 Every month, women who live in states that allow gender rating are made to pay higher premiums than men for the same coverage. Over time, this additional cost adds up. When average currently advertised premium prices are applied to the number of women who purchase individual insurance coverage, NWLC calculates that aggregately, women spend approximately $1 billion more for health coverage annually than they would if they were men, not counting any additional costs women must pay because of the exclusion of maternity benefits.

• Such wide variations in the ‘premium gender gap’ exist, both within and across states, that any actuarial justification is highly questionable.

NWLC found substantial differences in rates charged among comparable plans across the country. To do so, the Center selected plans with a similar set of features (i.e., similar cost-sharing and deductibles) that did not include maternity coverage and calculated the difference in premiums—or the ‘premium gender gap’—charged to women and men at ages 25, 40, and 55. As shown in Table 2, there are wide variations in the premium gaps charged to women and men for health plans with similar features, both within states and across the country. For example, one plan examined in Arkansas charges 25-year- old women 81% more than men for coverage while a similar plan in the same state only charges women 10% more for coverage than men.

• NWLC found that significant differences in the premium gender gap also exist across insurance companies. For example, one insurance company examined charges 40-year-old women an average of 20% more than men for the same coverage while another company charges women an average of 50% more than men for the same coverage.9

•

• Such wide variations in plans with very similar features suggest that it is not merely actuarial considerations driving the price differences.

•

Demo_Chris

(6,234 posts)lumberjack_jeff

(33,224 posts)about half of which is not attributable to maternity but to longer lifespans.

http://www.ncbi.nlm.nih.gov/pmc/articles/PMC1361028/

It's not a big woman-hating conspiracy, it's actuarial math. The contention that it was some kind of bigoted "cost of being female" is primarily a function of fundraising for organizations like NWLC.

pnwmom

(108,973 posts)Two plus two always equals four.

But in the case of health insurance, there is wide variation in the additional premiums women have been asked to pay. It can't be accounted for by increased maternity costs because individual policies hardly ever covered maternity costs -- women were being charged more for the same policies as men WITHOUT MATERNITY BENEFITS.

And the fact that women have longer lifespans -- that they live longer, healthier lives -- doesn't account for why they should pay a higher premium in any particular year.

lumberjack_jeff

(33,224 posts)and each state has regulatory rules which affect the premiums.

In general, everything else being equal, one would have expected women's premiums to be about 30% more than an equivalent man's premiums.

pnwmom

(108,973 posts)them free rein to hide extra profits behind women's supposedly extra costs. You are very trusting of the insurance companies to not be taking advantage of that.

And you already mentioned maternity benefits and women's longer life spans as being the reason for the supposedly 30% differential. But maternity benefits are routinely excluded, so they can't be the reason for the higher premiums. And the fact that a woman lives longer into her 80's doesn't justify charging her a higher premium during her 40th year.

lumberjack_jeff

(33,224 posts)Young men's insurance is going up because the higher cost to insure women, combined with the requirement that old people's insurance can't be more than 5x the price of young people's insurance.

Young men aren't paying for the average cost to insure young men. They're paying for the cost to insure young men and women, subject to the 5:1 ratio to near-retirees.

No free lunch, but the cost of it is shifted almost entirely onto young men, without much to show for it.

pnwmom

(108,973 posts)charged up till now can't be explained away by actuarial statistics; if they could, there would be some consistency across regions or among different insurers -- but instead there is a huge variation.

"For example, one plan examined in Arkansas charges 25-year- old women 81% more than men for coverage while a similar plan in the same state only charges women 10% more for coverage than men." (Link below)

And the fact that women sometimes need maternity benefits doesn't account for this because the overwhelming percent of individual policies for women didn't include ANY maternity benefits. They were being charged more than men for the exact same policies.

Now that insurers have been forced to give up their practice of hiding rate increases behind what everyone just seems to know -- that women supposedly cost that much more -- men's rates will be going up. C'est la vie. Up till now, women have been paying more than $1 billion more a year for the same coverage -- with maternity benefits excluded. The ACA finally fixed this. Selectively pulling out one major data point -- gender -- to rate people wasn't fair in the first place, and was obviously being misused by the insurance companies. If their rates were mathematically justified, then they wouldn't have had such wide variation.

OTOH, I think they should also get rid of gender rating with regard to auto insurance, and should no longer charge according to credit ratings, either. They should only be looking at driving education, driving history, and programs like voluntary participation in monitoring actual driving practices IMHO. (Our insurer has a program where you can pay them to install something in your car that will show them how you routinely drive it, and you can get significant refunds if you drive like a father in a minivan.)

National Women’s Law Center

http://www.nwlc.org/sites/default/files/pdfs/nwlc_2012_turningtofairness_report.pdf

The practice of gender rating is rampant in the individual market.

• The vast majority of insurance companies charge women significantly more than men, even with maternity coverage excluded.

• To assess the prevalence of gender rating among popular plans in the individual health insurance market, NWLC examined gender rating among best-selling plans on eHealthInsurance.com.

As shown in Table 1, the Center found that in the capital cities of states that permit gender rating, 92% of best-selling plans charge 40-year-old women more than 40-year- old men for identical coverage. Gender rating is highly prevalent across and within states. In 31 states, all of the best-selling plans engage in this unfair practice. Moreover, of the best-selling plans that gender rate in 2012, only 3% include maternity coverage in the individual health insurance policy. Therefore, overall, maternity coverage does not account for the extra amount that women must pay.

• Based on an average of currently advertised premiums and the most recent data on the number of women

in the individual health insurance market, the practice of gender rating costs women approximately $1 billion in a year.

There are approximately 7.5 million women who purchase health insurance in the individual market.8 Every month, women who live in states that allow gender rating are made to pay higher premiums than men for the same coverage. Over time, this additional cost adds up. When average currently advertised premium prices are applied to the number of women who purchase individual insurance coverage, NWLC calculates that aggregately, women spend approximately $1 billion more for health coverage annually than they would if they were men, not counting any additional costs women must pay because of the exclusion of maternity benefits.

• Such wide variations in the ‘premium gender gap’ exist, both within and across states, that any actuarial justification is highly questionable.

NWLC found substantial differences in rates charged among comparable plans across the country. To do so, the Center selected plans with a similar set of features (i.e., similar cost-sharing and deductibles) that did not include maternity coverage and calculated the difference in premiums—or the ‘premium gender gap’—charged to women and men at ages 25, 40, and 55. As shown in Table 2, there are wide variations in the premium gaps charged to women and men for health plans with similar features, both within states and across the country. For example, one plan examined in Arkansas charges 25-year- old women 81% more than men for coverage while a similar plan in the same state only charges women 10% more for coverage than men.

• NWLC found that significant differences in the premium gender gap also exist across insurance companies. For example, one insurance company examined charges 40-year-old women an average of 20% more than men for the same coverage while another company charges women an average of 50% more than men for the same coverage.9

•

• Such wide variations in plans with very similar features suggest that it is not merely actuarial considerations driving the price differences.

•

eridani

(51,907 posts)They do this because if all goes well, they will eventually become old people. Fucking around over who deserves what just adds expensive administrative nonsense to the system and wastes the money that could be used for health care for young and old alike.

CreekDog

(46,192 posts)the ones that say women's maternity coverage should be optional in these policies.

that's what I'm addressing.

you're so clueless you think that making premiums gender neutral makes is some affront to single payer.

wake up. i want single payer too.

but mistreating women is not the way to get there in the interim.

Bernie Sanders is to the left of you and has supported this in the absence of something better. don't try out outpious everyone on this topic.

eridani

(51,907 posts)--by single payer.

badtoworse

(5,957 posts)I would however point out that cancer and heart disease can strike young people as well. My brother was 45 when he died of cancer - that's not young, but it's not old either. Sadly, childhood cancers occur that take numerous lives each year and are expensive to treat. For that reason, I don't believe it would be prudent for a young person to have cancer or other serious diseases excluded from their coverage.

On average though, most of a person's lifetime healthcare expenses will occur in the last few years of their life.

Nuclear Unicorn

(19,497 posts)Treatment for obesity, substance abuse rehab, etc.?

CreekDog

(46,192 posts)why are you even wanting insurance. you're saying you're not fat, so you don't want to be in the pool with them.

well maybe they don't want to contribute to insuring you because you run or exercise daily and might get hit by a car or something.

if you want to be part of a group insurance pool, your risks are covered by others as they cover your risks, many of which they don't share.

if that's really your issue, i suggest you just use your bank account for all your insurance needs. if you are so healthy and don't need others to be in the group with you --then i just suggest you insure yourself, pay all your medical costs

and forego insurance because it's clear you don't want or understand insurance.

Nuclear Unicorn

(19,497 posts)Nothing says I have to carry rehab coverage except a law which can be changed. It's merely a construct.

I see no reason to subsidize someone else's bad behavior. Yes, maybe I might be hurt during exercise but that is happenstance, compared to someone else willfully engaging in behaviors known to be high risk.

CreekDog

(46,192 posts)take your pick.

if you want to cherrypick what will be covered of others, they can cherrypick what they participate in of your coverage.

ultimately, that's where insurance falls apart.

you think you can have it both ways.

insure yourself. period. that's what you want.

Nuclear Unicorn

(19,497 posts)People-who-don't-engage-in-self-destructive-behaviors-so-pay-lower-premiums group? That group could exist if silly people hadn't decreed otherwise.

My life insurance is lower because of my personal habits and I'll absolutely be using that some day.

CreekDog

(46,192 posts)what if the insurance company doesn't want to cover you for X, Y or Z?

do you support that?

Nuclear Unicorn

(19,497 posts)The law is merely a human construct. The fact that it is law speaks nothing about its wisdom -- or lack thereof. Your argument is nothing more than an appeal to authoritarianism.

do you support that?

We aren't talking about what insurance companies do or don't do. We're talking about your silly OP that says people who don't accept your authoritarianism should be denied the right to freely enter into a contract to their own benefit. I want a contract where I am not subsidizing other people's bad habits they took upon themselves. You, however, demand fealty to your silly dictates for no reason other than they're your silly dictates.

CreekDog

(46,192 posts)it is.

you want a system that allows discrimination in pricing so that your health insurance covers you but you aren't grouped with people that have different health care risks.

you advocate going around any system that benefits anyone else so that you can have your own individual policy that benefits you alone.

yeah, that's almost trolling the topic.

Nuclear Unicorn

(19,497 posts)Of course authoritarians hate independent thinking and react poorly to being challenged.

How about non-smokers being allowed to price policies based on their natural health risks and not being forced to subsidize people who choose to engage in a known unhealthy habit?

Please give me one good reason why I have to subsidize their risks while they get to have a benefit with no commensurate imposition. Your system actually penalizes healthy lifestyles. Do bad? Break even. Do good? pay more with no tangible return; not even the benefit of an honest dialogue just, "Shut up! That's why!"

solarhydrocan

(551 posts)I'd bet very few of those that talk about "discrimination" are upset even a bit about smokers being charged more for mandated insurance.

Hopefully it's just a matter of time before dietary choices will be treated the same.

Everyone can find something to hate about someone else- and now that we are all involved by mandate to care about what all of us eats, drinks or smokes this train is about to leave the station. "All Aboard!"

CreekDog

(46,192 posts)or chronically ill who are in such conditions through no fault of their own?

Emelina

(188 posts)Why should a fit person who strives to remain healthy have to pay higher costs to subsidize those obese people you see at Walmart who are too huge to even walk to shop? Why should people who eat organic, do not smoke or even drink have to pay for people who just don't care what they do to their bodies?

Lars39

(26,109 posts)Whereas the rest of us could live into our nineties.

CreekDog

(46,192 posts)but if they can't afford the insurance, because you won't be in a group with them, they won't pay anything.

so who will pay for their care? you alone.

you think you're saving money by not being in a group with them.

in reality, you're costing yourself more that way.

counter intuitive, i know.

by the way, that's some selfish shit you're peddling.

mainer

(12,022 posts)and that spinal cord injury, with a lifetime of paralysis, will cost way more than the obese guy's healthcare costs.

retread

(3,761 posts)available.

Coyotl

(15,262 posts)The whole idea of insurance is to spread the risk. The fact that young people will be old people someday factors in to spreading the risk of entire lifetimes to the entire pool.

mike_c

(36,281 posts)Seriously. Pooled risk is what insurance is. I loathe the insurance industry, and would love to see them kicked to the curb of history, but anyone who buys insurance does so to pool their risks with other peoples' risks. That is what medical insurance is. Complaining about other peoples' risks in one's own pool makes no sense at all. People who don't want to pool their risks with others should not buy medical insurance.