Welcome to DU!

The truly grassroots left-of-center political community where regular people, not algorithms, drive the discussions and set the standards.

Join the community:

Create a free account

Support DU (and get rid of ads!):

Become a Star Member

Latest Breaking News

General Discussion

The DU Lounge

All Forums

Issue Forums

Culture Forums

Alliance Forums

Region Forums

Support Forums

Help & Search

Economy

In reply to the discussion: Weekend Economists Waiting for FDR July 13-15, 2012 [View all]Demeter

(85,373 posts)21. So How Much Did the Banksters Make on Libor-Related Ill-Gotten Gains?

http://www.nakedcapitalism.com/2012/07/so-how-much-did-the-banksters-make-on-libor-related-ill-gotten-gains.html?utm_source=feedburner&utm_medium=email&utm_campaign=Feed%3A+NakedCapitalism+%28naked+capitalism%29

...The Morgan Stanley estimate, which dors an admirable job of trying to dimension what the damage might be (this is admittedly a pretty fraught exercise) looks at different categories of exposure. First is regulatory fines, which it ballparks at $850 million for Bank of America, Citi and JP Morgan, and a mere $550 millionish for Lloyds. Next is litigation risk, which it sees averaging $440 million per bank, with the hit for each ranging from $60 million to $1.1 billion. It finally flags, but does not cost out, the fact that banks will be forced to change how they do business going forward. If the Libor revelations lead to more transparency, not just in Libor but other areas, that could have a significant impact. Banks enjoy a tremendous advantage over customers in markets where pricing is opaque.

But what about the bonuses that all the staff got as a result of this nefarious activity? The inability to recoup those payouts is a big reason to be skeptical that anything will change, ex much more aggressive supervision and disclosure, or maybe (gasp) prosecutions. And so far, despite the enormous costs of the crisis, the banks have done a good job in limiting reforms (I don’t take their caviling that their lower profits are due to regulation seriously. Damage your customers on a massive basis by blowing up the global economy, and lose your cheap float profits due to central bank ZIRP policies to prop up your balance sheets, and what do you expect?).

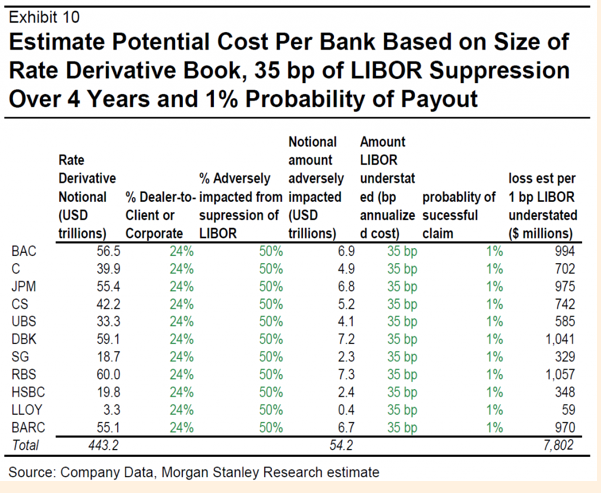

Morgan Stanley provides an estimate of the impact of Libor suppression, 35 basis points for each year, 2007 to 2011 (see exhibit 10, third column from the right). That level is consistent with NC reader complaints during the criss (go NC readers!). I’m surprised that it would have continued at that level post, say, early 2009, but we’ll assume four years.

...The Morgan Stanley estimate, which dors an admirable job of trying to dimension what the damage might be (this is admittedly a pretty fraught exercise) looks at different categories of exposure. First is regulatory fines, which it ballparks at $850 million for Bank of America, Citi and JP Morgan, and a mere $550 millionish for Lloyds. Next is litigation risk, which it sees averaging $440 million per bank, with the hit for each ranging from $60 million to $1.1 billion. It finally flags, but does not cost out, the fact that banks will be forced to change how they do business going forward. If the Libor revelations lead to more transparency, not just in Libor but other areas, that could have a significant impact. Banks enjoy a tremendous advantage over customers in markets where pricing is opaque.

But what about the bonuses that all the staff got as a result of this nefarious activity? The inability to recoup those payouts is a big reason to be skeptical that anything will change, ex much more aggressive supervision and disclosure, or maybe (gasp) prosecutions. And so far, despite the enormous costs of the crisis, the banks have done a good job in limiting reforms (I don’t take their caviling that their lower profits are due to regulation seriously. Damage your customers on a massive basis by blowing up the global economy, and lose your cheap float profits due to central bank ZIRP policies to prop up your balance sheets, and what do you expect?).

Morgan Stanley provides an estimate of the impact of Libor suppression, 35 basis points for each year, 2007 to 2011 (see exhibit 10, third column from the right). That level is consistent with NC reader complaints during the criss (go NC readers!). I’m surprised that it would have continued at that level post, say, early 2009, but we’ll assume four years.

Edit history

Please sign in to view edit histories.

69 replies

= new reply since forum marked as read

Highlight:

NoneDon't highlight anything

5 newestHighlight 5 most recent replies

RecommendedHighlight replies with 5 or more recommendations

= new reply since forum marked as read

Highlight:

NoneDon't highlight anything

5 newestHighlight 5 most recent replies

RecommendedHighlight replies with 5 or more recommendations

= new reply since forum marked as read

Highlight:

NoneDon't highlight anything

5 newestHighlight 5 most recent replies

RecommendedHighlight replies with 5 or more recommendations

Corporations Dodge LIBOR Scandal Bullet: Its banks and hedge funds that look like the losers.

Demeter

Jul 2012

#34

Unfortunately, they're probabaly right that it'll take a long time to sort out the consequences; but

snot

Jul 2012

#59

How Out-of-Control Credit Markets Threaten Liberty, Democracy and Economic Security By Ed Harrison

Demeter

Jul 2012

#30

The Great Capitalist Heist: How Paris Hiltons Dogs Ended Up Better Off Than You

Demeter

Jul 2012

#35

Another "this should be a separate thread", and what of the outcome for this repeat? I'd love to

mother earth

Jul 2012

#39