| Latest | Greatest | Lobby | Journals | Search | Options | Help | Login |

|

|

|

This topic is archived. |

| Home » Discuss » Latest Breaking News |

|

| Demeter

|

Mon Apr-07-08 06:32 AM Original message |

| STOCK MARKET WATCH, Monday April 7, 2008 |

| Printer Friendly | Permalink | | Top |

| Demeter

|

Mon Apr-07-08 06:34 AM Response to Original message |

| 1. Since Ozy Hasn't Yet....Here It Is! |

| Printer Friendly | Permalink | | Top |

| DemReadingDU

|

Mon Apr-07-08 07:07 AM Response to Reply #1 |

| 17. Thank you! |

| Printer Friendly | Permalink | | Top |

| Hugin

|

Mon Apr-07-08 10:26 AM Response to Reply #1 |

| 58. Thanks Demeter. |

| Printer Friendly | Permalink | | Top |

| Demeter

|

Mon Apr-07-08 06:35 AM Response to Original message |

| 2. Today's Reports |

| Printer Friendly | Permalink | | Top |

| UpInArms

|

Mon Apr-07-08 03:17 PM Response to Reply #2 |

| 89. U.S. Feb. consumer credit rises $5.2 billion, or 2.4% rate |

| Printer Friendly | Permalink | | Top |

| JNelson6563

|

Mon Apr-07-08 06:36 AM Response to Original message |

| 3. Where are my shades? Gosh those futures are bright! |

| Printer Friendly | Permalink | | Top |

| Demeter

|

Mon Apr-07-08 08:51 AM Response to Reply #3 |

| 42. Didn't Last Long, Did It? |

| Printer Friendly | Permalink | | Top |

| RawMaterials

|

Mon Apr-07-08 10:52 AM Response to Reply #3 |

| 66. I have been thinking about this McSame stuff |

| Printer Friendly | Permalink | | Top |

| Demeter

|

Mon Apr-07-08 06:38 AM Response to Original message |

| 4. A Brief Technical Update BY TIM W. WOOD |

| Printer Friendly | Permalink | | Top |

| Ghost Dog

|

Mon Apr-07-08 06:38 AM Response to Original message |

| 5. GLOBAL MARKETS WEEKAHEAD - G7 rescue plan dominates investors |

| Printer Friendly | Permalink | | Top |

| Ghost Dog

|

Mon Apr-07-08 06:39 AM Response to Reply #5 |

| 6. - Dollar up on equity bounce, narrower credit spreads |

| Printer Friendly | Permalink | | Top |

| Ghost Dog

|

Mon Apr-07-08 06:41 AM Response to Reply #5 |

| 7. - World stocks power to one-month high |

| Printer Friendly | Permalink | | Top |

| Ghost Dog

|

Mon Apr-07-08 06:42 AM Response to Reply #7 |

| 8. - Nikkei at 5-week closing high as resource firms gain |

| Printer Friendly | Permalink | | Top |

| Ghost Dog

|

Mon Apr-07-08 06:57 AM Response to Reply #8 |

| 12. Asian Stocks Rise to Five-Week High, Led by BHP; ANZ Tumbles |

| Printer Friendly | Permalink | | Top |

| Ghost Dog

|

Mon Apr-07-08 06:43 AM Response to Reply #7 |

| 9. - European shares rise early, driven by miners, M&A |

| Printer Friendly | Permalink | | Top |

| Ghost Dog

|

Mon Apr-07-08 07:01 AM Response to Reply #5 |

| 14. Rice Run Prompts Curbs to Rival Credit Market Seizure |

| Printer Friendly | Permalink | | Top |

| UpInArms

|

Mon Apr-07-08 06:52 AM Response to Original message |

| 10. dollar watch |

| Printer Friendly | Permalink | | Top |

| Demeter

|

Mon Apr-07-08 11:22 AM Response to Reply #10 |

| 73. Hopes of Continued Dollar Rally Fading |

| Printer Friendly | Permalink | | Top |

| Demeter

|

Mon Apr-07-08 06:53 AM Response to Original message |

| 11. Oil rises on prospects for more Fed cuts By PABLO GORONDI, AP |

| Printer Friendly | Permalink | | Top |

| UpInArms

|

Mon Apr-07-08 07:37 AM Response to Reply #11 |

| 26. U.S. gasoline prices rise to almost $3.32/gallon |

| Printer Friendly | Permalink | | Top |

| UpInArms

|

Mon Apr-07-08 07:38 AM Response to Reply #11 |

| 27. Iran to OPEC: Stop oil sales in dollars |

| Printer Friendly | Permalink | | Top |

| mdmc

|

Mon Apr-07-08 10:32 AM Response to Reply #27 |

| 59. Uh no! |

| Printer Friendly | Permalink | | Top |

| UpInArms

|

Mon Apr-07-08 03:18 PM Response to Reply #11 |

| 90. (OMG!) Crude closes up $2.86, or 2.7%, to $109.09 a barrel |

| Printer Friendly | Permalink | | Top |

| UpInArms

|

Mon Apr-07-08 06:58 AM Response to Original message |

| 13. Hedge fund managers make mint on housing crisis |

| Printer Friendly | Permalink | | Top |

| Demeter

|

Mon Apr-07-08 07:01 AM Response to Reply #13 |

| 15. $3 BILLION??? |

| Printer Friendly | Permalink | | Top |

| Tansy_Gold

|

Mon Apr-07-08 08:09 AM Response to Reply #15 |

| 35. Correct me if I'm wrong. . . . . |

| Printer Friendly | Permalink | | Top |

| scisyhp1

|

Mon Apr-07-08 09:50 AM Response to Reply #35 |

| 52. That would be the taxpayers. Letting the Bear Stearns shareholders |

| Printer Friendly | Permalink | | Top |

| Tansy_Gold

|

Mon Apr-07-08 10:24 AM Response to Reply #52 |

| 57. Oh, course! Silly me! Why didn't I figure that out? |

| Printer Friendly | Permalink | | Top |

| Demeter

|

Mon Apr-07-08 07:06 AM Response to Original message |

| 16. Wall St banks 'hooked on emergency funds scheme' |

| Printer Friendly | Permalink | | Top |

| Demeter

|

Mon Apr-07-08 07:21 AM Response to Reply #16 |

| 21. Demythologizing Central Bankers and the Great Moderation |

| Printer Friendly | Permalink | | Top |

| Tansy_Gold

|

Mon Apr-07-08 08:13 AM Response to Reply #16 |

| 37. HA HA HA HA HA HA HA HA HA HA HA HA |

| Printer Friendly | Permalink | | Top |

| Demeter

|

Mon Apr-07-08 08:32 AM Response to Reply #37 |

| 39. You're Such a Card, Tansy Gold! |

| Printer Friendly | Permalink | | Top |

| TalkingDog

|

Mon Apr-07-08 11:45 AM Response to Reply #37 |

| 76. Create a Meme contest: Old and Busted - Welfare Queens. |

| Printer Friendly | Permalink | | Top |

| Demeter

|

Mon Apr-07-08 12:00 PM Response to Reply #76 |

| 79. I'm Glad I Could, But Worried. Where's Ozy? |

| Printer Friendly | Permalink | | Top |

| burf

|

Mon Apr-07-08 12:35 PM Response to Reply #76 |

| 80. Wall Street Welfare Club |

| Printer Friendly | Permalink | | Top |

| AnneD

|

Mon Apr-07-08 01:45 PM Response to Reply #80 |

| 83. Memo Contest..... |

| Printer Friendly | Permalink | | Top |

| Hugin

|

Mon Apr-07-08 03:27 PM Response to Reply #76 |

| 92. "Welfare Barons" |

| Printer Friendly | Permalink | | Top |

| MilesColtrane

|

Mon Apr-07-08 09:00 AM Response to Reply #16 |

| 45. There's the moral hazard of the Fed bailing Bear Stearns. |

| Printer Friendly | Permalink | | Top |

| Hugin

|

Mon Apr-07-08 10:38 AM Response to Reply #16 |

| 61. It seems to me that just a couple of days worth would put the whole 'Sub-Prime'... |

| Printer Friendly | Permalink | | Top |

| AnneD

|

Mon Apr-07-08 10:51 AM Response to Reply #16 |

| 65. I guess in Chopper Ben education he never read the scholarly tome... |

| Printer Friendly | Permalink | | Top |

| Demeter

|

Mon Apr-07-08 07:10 AM Response to Original message |

| 18. The Chop Shop Economy: Other People's Money By ALAN FARAGO |

| Printer Friendly | Permalink | | Top |

| Tansy_Gold

|

Mon Apr-07-08 08:36 AM Response to Reply #18 |

| 41. "It's the history, stupid." |

| Printer Friendly | Permalink | | Top |

| wordpix

|

Mon Apr-07-08 03:52 PM Response to Reply #18 |

| 93. I do not trust what BushCo has put up as collateral to borrow heavily, totaling $9.2 trillion debt |

| Printer Friendly | Permalink | | Top |

| DemReadingDU

|

Mon Apr-07-08 07:11 AM Response to Original message |

| 19. Bonddad: The Bush Boom Was a Complete Bust |

| Printer Friendly | Permalink | | Top |

| DemReadingDU

|

Mon Apr-07-08 07:15 AM Response to Original message |

| 20. Max Keiser: Fixing the Problems on Wall Street is Easy: Raise Margin Requirements |

| Printer Friendly | Permalink | | Top |

| DemReadingDU

|

Mon Apr-07-08 07:24 AM Response to Original message |

| 22. Bill Fleckenstein: Our housing-bubble hangover |

| Printer Friendly | Permalink | | Top |

| Demeter

|

Mon Apr-07-08 07:28 AM Response to Original message |

| 23. Road for electric car makers full of potholes By Ken Bensinger Los Angeles Times Staff Writer |

| Printer Friendly | Permalink | | Top |

| Demeter

|

Mon Apr-07-08 07:30 AM Response to Original message |

| 24. Credit Card Redlining by Adam Levitin |

| Printer Friendly | Permalink | | Top |

| DemReadingDU

|

Mon Apr-07-08 07:31 AM Response to Original message |

| 25. Mike Whitney: Fed Up: Bernanke joins G-7 to Stem Global Financial Meltdown |

| Printer Friendly | Permalink | | Top |

| Demeter

|

Mon Apr-07-08 07:48 AM Response to Reply #25 |

| 30. READ THE WHOLE ARTICLE! |

| Printer Friendly | Permalink | | Top |

| DemReadingDU

|

Mon Apr-07-08 08:55 AM Response to Reply #30 |

| 44. Reading Mike Whitney is like reading a small novel |

| Printer Friendly | Permalink | | Top |

| Hugin

|

Mon Apr-07-08 10:43 AM Response to Reply #30 |

| 62. Oh! Oh! Pick me! Oh Oh!... |

| Printer Friendly | Permalink | | Top |

| Demeter

|

Mon Apr-07-08 11:06 AM Response to Reply #62 |

| 68. Okay Prag, Since Bueller Isn't Here-- |

| Printer Friendly | Permalink | | Top |

| Hugin

|

Mon Apr-07-08 11:11 AM Response to Reply #68 |

| 69. Uh... Umm... Umm... |

| Printer Friendly | Permalink | | Top |

| Demeter

|

Mon Apr-07-08 11:14 AM Response to Reply #69 |

| 71. A Greater Depression, Of Couse! |

| Printer Friendly | Permalink | | Top |

| DemReadingDU

|

Mon Apr-07-08 04:28 PM Response to Reply #71 |

| 97. If the Democrats win the Presidency and get 60+ in the Senate |

| Printer Friendly | Permalink | | Top |

| Demeter

|

Mon Apr-07-08 05:12 PM Response to Reply #97 |

| 99. We Can Hope He Isn't Reappointed |

| Printer Friendly | Permalink | | Top |

| donkeyotay

|

Mon Apr-07-08 10:51 AM Response to Reply #25 |

| 64. Read the whole article! |

| Printer Friendly | Permalink | | Top |

| Tansy_Gold

|

Mon Apr-07-08 01:59 PM Response to Reply #64 |

| 84. "These over-leveraged banking behemoths need to fail." |

| Printer Friendly | Permalink | | Top |

| Tansy_Gold

|

Mon Apr-07-08 01:42 PM Response to Reply #25 |

| 82. Hey, folks! Look over here! |

| Printer Friendly | Permalink | | Top |

| DemReadingDU

|

Mon Apr-07-08 04:19 PM Response to Reply #82 |

| 95. Best sentence in the article! |

| Printer Friendly | Permalink | | Top |

| wordpix

|

Mon Apr-07-08 04:21 PM Response to Reply #25 |

| 96. "the logical conclusion that the banking system is bankrupt"--how about the FEDERAL system? |

| Printer Friendly | Permalink | | Top |

| DemReadingDU

|

Mon Apr-07-08 07:40 AM Response to Original message |

| 28. Dana Milbank: Meet Alan Schwartz, welfare recipient. |

| Printer Friendly | Permalink | | Top |

| Demeter

|

Mon Apr-07-08 07:41 AM Response to Original message |

| 29. A Brighter Spotlight, Yet the Pay Rises By CLAUDIA H. DEUTSCH |

| Printer Friendly | Permalink | | Top |

| Demeter

|

Mon Apr-07-08 07:58 AM Response to Original message |

| 31. Bear/JP Morgan: The Rashomon Defense |

| Printer Friendly | Permalink | | Top |

| Demeter

|

Mon Apr-07-08 08:02 AM Response to Original message |

| 32. Banks Backlogged by Foreclosures, Let Defaulting Borrowers Stay in Homes |

| Printer Friendly | Permalink | | Top |

| Demeter

|

Mon Apr-07-08 08:06 AM Response to Reply #32 |

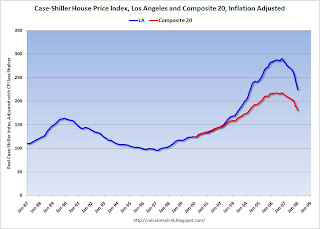

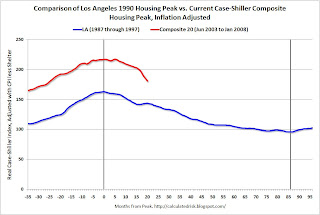

| 33. Housing Bust Duration |

| Printer Friendly | Permalink | | Top |

| Demeter

|

Mon Apr-07-08 08:08 AM Response to Reply #33 |

| 34. "The next time we have Black Monday" |

| Printer Friendly | Permalink | | Top |

| Tansy_Gold

|

Mon Apr-07-08 10:35 AM Response to Reply #34 |

| 60. S&L history, RTC, Lincoln Savings, Charles Keating, etc. |

| Printer Friendly | Permalink | | Top |

| wordpix

|

Mon Apr-07-08 04:18 PM Response to Reply #33 |

| 94. thanks for that. I bought my condo in '98 near the end of previous bust & start of the 2000's boom |

| Printer Friendly | Permalink | | Top |

| Demeter

|

Mon Apr-07-08 05:15 PM Response to Reply #94 |

| 100. So Just Wait a Couple of Years |

| Printer Friendly | Permalink | | Top |

| Demeter

|

Mon Apr-07-08 08:12 AM Response to Original message |

| 36. A BAD TRADE by Bill Bonner |

| Printer Friendly | Permalink | | Top |

| Demeter

|

Mon Apr-07-08 08:30 AM Response to Original message |

| 38. The Bottoms Are In - Or Are They? |

| Printer Friendly | Permalink | | Top |

| AnneD

|

Mon Apr-07-08 09:06 AM Response to Reply #38 |

| 46. It is that comment..... |

| Printer Friendly | Permalink | | Top |

| AnneD

|

Mon Apr-07-08 08:33 AM Response to Original message |

| 40. Morning Marketeers...... |

| Printer Friendly | Permalink | | Top |

| Demeter

|

Mon Apr-07-08 08:55 AM Response to Reply #40 |

| 43. Morning, AnneD |

| Printer Friendly | Permalink | | Top |

| AnneD

|

Mon Apr-07-08 09:15 AM Response to Original message |

| 47. Some good news...sort of |

| Printer Friendly | Permalink | | Top |

| AnneD

|

Mon Apr-07-08 09:24 AM Response to Original message |

| 48. Report: WaMu close to $5B infusion |

| Printer Friendly | Permalink | | Top |

| AnneD

|

Mon Apr-07-08 09:34 AM Response to Reply #48 |

| 50. Put this on your radar screen....... |

| Printer Friendly | Permalink | | Top |

| Demeter

|

Mon Apr-07-08 11:00 AM Response to Reply #48 |

| 67. TPG to Invest $5 Billion in Wamu--Naked Capitalism Commentary |

| Printer Friendly | Permalink | | Top |

| nichomachus

|

Mon Apr-07-08 09:29 AM Response to Original message |

| 49. If you adjust for inflation |

| Printer Friendly | Permalink | | Top |

| Demeter

|

Mon Apr-07-08 09:48 AM Response to Reply #49 |

| 51. It's Not Even the Same DOW |

| Printer Friendly | Permalink | | Top |

| slipslidingaway

|

Mon Apr-07-08 12:37 PM Response to Reply #51 |

| 81. Since Bush took office... |

| Printer Friendly | Permalink | | Top |

| Wednesdays

|

Mon Apr-07-08 09:51 AM Response to Reply #49 |

| 53. Link? |

| Printer Friendly | Permalink | | Top |

| DemReadingDU

|

Mon Apr-07-08 09:57 AM Response to Reply #53 |

| 54. The Real Dow |

| Printer Friendly | Permalink | | Top |

| nichomachus

|

Mon Apr-07-08 10:06 AM Response to Reply #54 |

| 55. And if you count real inflation |

| Printer Friendly | Permalink | | Top |

| DemReadingDU

|

Mon Apr-07-08 10:16 AM Response to Reply #55 |

| 56. inflation, higher prices |

| Printer Friendly | Permalink | | Top |

| Hugin

|

Mon Apr-07-08 10:48 AM Response to Reply #49 |

| 63. Thanks for pointing that out nichomachus... |

| Printer Friendly | Permalink | | Top |

| Demeter

|

Mon Apr-07-08 11:12 AM Response to Original message |

| 70. The Manic-Depressive Market |

| Printer Friendly | Permalink | | Top |

| Demeter

|

Mon Apr-07-08 11:20 AM Response to Original message |

| 72. Central banks are dangerous |

| Printer Friendly | Permalink | | Top |

| Demeter

|

Mon Apr-07-08 11:43 AM Response to Original message |

| 74. Mortgage Bankers Association struggles to pay its mortgage |

| Printer Friendly | Permalink | | Top |

| Demeter

|

Mon Apr-07-08 11:44 AM Response to Original message |

| 75. Prag, We Need Another Goose Report |

| Printer Friendly | Permalink | | Top |

| Hugin

|

Mon Apr-07-08 02:46 PM Response to Reply #75 |

| 87. I'll check... |

| Printer Friendly | Permalink | | Top |

| Hugin

|

Mon Apr-07-08 03:25 PM Response to Reply #75 |

| 91. "U.S. Treasury balances at Fed higher on April 4" |

| Printer Friendly | Permalink | | Top |

| Demeter

|

Mon Apr-07-08 11:53 AM Response to Original message |

| 77. Gold futures soar 2%; other metals also rise By Polya Lesova, MarketWatch |

| Printer Friendly | Permalink | | Top |

| Demeter

|

Mon Apr-07-08 11:59 AM Response to Original message |

| 78. Stocks rise on hopes for financial recovery |

| Printer Friendly | Permalink | | Top |

| TalkingDog

|

Mon Apr-07-08 02:05 PM Response to Original message |

| 85. Seems the Fashionistas knew before Shrub & Co. |

| Printer Friendly | Permalink | | Top |

| AnneD

|

Mon Apr-07-08 02:24 PM Response to Original message |

| 86. Novartis buys stake in Alcon, eyes full takeover |

| Printer Friendly | Permalink | | Top |

| TalkingDog

|

Mon Apr-07-08 03:09 PM Response to Original message |

| 88. 1.71?!!! Really? All they can manage is the same stakes as penny poker? |

| Printer Friendly | Permalink | | Top |

| Demeter

|

Mon Apr-07-08 05:06 PM Response to Original message |

| 98. To Go With the Vaudevillian, Rollercoaster Ride, Might I Propose Today's Theme? |

| Printer Friendly | Permalink | | Top |

| Hugin

|

Mon Apr-07-08 07:41 PM Response to Reply #98 |

| 103. Great choice! |

| Printer Friendly | Permalink | | Top |

| Wednesdays

|

Mon Apr-07-08 05:32 PM Response to Original message |

| 101. And today's headline: Dow Closes in Positive Territory!! |

| Printer Friendly | Permalink | | Top |

| UpInArms

|

Mon Apr-07-08 06:26 PM Response to Original message |

| 102. closing numbers and blather |

| Printer Friendly | Permalink | | Top |

| DU

AdBot (1000+ posts) |

Fri Apr 26th 2024, 10:37 AM Response to Original message |

| Advertisements [?] |

| Top |

| Home » Discuss » Latest Breaking News |

|

Powered by DCForum+ Version 1.1 Copyright 1997-2002 DCScripts.com

Software has been extensively modified by the DU administrators

Important Notices: By participating on this discussion board, visitors agree to abide by the rules outlined on our Rules page. Messages posted on the Democratic Underground Discussion Forums are the opinions of the individuals who post them, and do not necessarily represent the opinions of Democratic Underground, LLC.

Home | Discussion Forums | Journals | Store | Donate

About DU | Contact Us | Privacy Policy

Got a message for Democratic Underground? Click here to send us a message.

© 2001 - 2011 Democratic Underground, LLC