| Latest | Greatest | Lobby | Journals | Search | Options | Help | Login |

|

|

|

This topic is archived. |

| Home » Discuss » Editorials & Other Articles |

|

| Demeter

|

Fri Sep-19-08 06:50 PM Original message |

| The Weekend Economist September 19-21, 2008 |

| Printer Friendly | Permalink | | Top |

| Demeter

|

Fri Sep-19-08 06:56 PM Response to Original message |

| 1. Morgan Stanley in talks with CIC |

| Printer Friendly | Permalink | | Top |

| Tansy_Gold

|

Sat Sep-20-08 02:44 PM Response to Reply #1 |

| 76. Can someone explain to me. . .. . |

| Printer Friendly | Permalink | | Top |

| Demeter

|

Sat Sep-20-08 05:59 PM Response to Reply #76 |

| 81. All Too Probable, Tansy |

| Printer Friendly | Permalink | | Top |

| Tansy_Gold

|

Sat Sep-20-08 07:04 PM Response to Reply #81 |

| 84. My point exactly. |

| Printer Friendly | Permalink | | Top |

| Hugin

|

Sun Sep-21-08 02:27 AM Response to Reply #76 |

| 95. I'm glad you're around to say what I'm thinking. nt |

| Printer Friendly | Permalink | | Top |

| Tansy_Gold

|

Sun Sep-21-08 07:01 AM Response to Reply #95 |

| 104. LOL -- well, at least we can still THINK |

| Printer Friendly | Permalink | | Top |

| Hugin

|

Sun Sep-21-08 09:08 AM Response to Reply #104 |

| 119. Is this in your journal? |

| Printer Friendly | Permalink | | Top |

| Tansy_Gold

|

Sun Sep-21-08 09:13 AM Response to Reply #119 |

| 120. I always forget about that. |

| Printer Friendly | Permalink | | Top |

| Hugin

|

Sun Sep-21-08 10:42 AM Response to Reply #120 |

| 126. I tried to update my Simulacrum last week. |

| Printer Friendly | Permalink | | Top |

| Demeter

|

Fri Sep-19-08 06:59 PM Response to Original message |

| 2. Buffett in $4.7bn deal for Constellation |

| Printer Friendly | Permalink | | Top |

| Demeter

|

Fri Sep-19-08 07:02 PM Response to Original message |

| 3. Five banks exploring WaMu records |

| Printer Friendly | Permalink | | Top |

| ozymandius

|

Fri Sep-19-08 07:02 PM Response to Original message |

| 4. Should you need any other reason to despise Gramm and McCain... |

| Printer Friendly | Permalink | | Top |

| ozymandius

|

Fri Sep-19-08 07:08 PM Response to Original message |

| 5. U.S. regulators close W. Va bank; 12th to fail |

| Printer Friendly | Permalink | | Top |

| Demeter

|

Fri Sep-19-08 07:11 PM Response to Reply #5 |

| 7. Good Catch, Ozy! |

| Printer Friendly | Permalink | | Top |

| Demeter

|

Fri Sep-19-08 07:10 PM Response to Original message |

| 6. Blast From The Past: Last Wednesday, to Be Precise! |

| Printer Friendly | Permalink | | Top |

| Demeter

|

Fri Sep-19-08 07:22 PM Response to Original message |

| 8. A Mark Fiore Perspective |

| Printer Friendly | Permalink | | Top |

| Demeter

|

Fri Sep-19-08 07:32 PM Response to Original message |

| 9. Benjamin R. Barber: The Fiscal Meltdown Reveals the Democratic Deficit |

| Printer Friendly | Permalink | | Top |

| Demeter

|

Fri Sep-19-08 07:34 PM Response to Original message |

| 10. MAN UNITED.... |

| Printer Friendly | Permalink | | Top |

| UpInArms

|

Fri Sep-19-08 07:37 PM Response to Original message |

| 11. (Hedge Fund) Reserve seeks to halt fund redemptions; investors flee |

| Printer Friendly | Permalink | | Top |

| Demeter

|

Fri Sep-19-08 07:40 PM Response to Original message |

| 12. Ban on Short-Selling Will Hurt Rather Than Help Broker-Dealers |

| Printer Friendly | Permalink | | Top |

| progressive_realist

|

Fri Sep-19-08 10:25 PM Response to Reply #12 |

| 35. The law of unintended consequences |

| Printer Friendly | Permalink | | Top |

| Tansy_Gold

|

Sat Sep-20-08 02:47 PM Response to Reply #12 |

| 77. It was only one segment of Carlyle. A mortgage-related |

| Printer Friendly | Permalink | | Top |

| Ghost Dog

|

Sun Sep-21-08 02:39 AM Response to Reply #77 |

| 96. It was Carlyle Capital Corp, an Amsterdam-based fund |

| Printer Friendly | Permalink | | Top |

| Tansy_Gold

|

Sun Sep-21-08 07:01 AM Response to Reply #96 |

| 105. I knew someone would find it! |

| Printer Friendly | Permalink | | Top |

| Demeter

|

Sun Sep-21-08 11:10 AM Response to Reply #77 |

| 129. Darn! And I Had My Hopes Up! |

| Printer Friendly | Permalink | | Top |

| Demeter

|

Fri Sep-19-08 07:48 PM Response to Original message |

| 13. Arianna Huffington: How Obama Can Demonstrate Real Leadership on the Economic Crisis |

| Printer Friendly | Permalink | | Top |

| RUMMYisFROSTED

|

Fri Sep-19-08 08:12 PM Response to Reply #13 |

| 19. Rubin and Summers are catching a lot of shit lately. |

| Printer Friendly | Permalink | | Top |

| Joe Chi Minh

|

Sat Sep-20-08 02:09 PM Response to Reply #13 |

| 71. Bull's-eye to bull's-eye. Good find. |

| Printer Friendly | Permalink | | Top |

| Demeter

|

Fri Sep-19-08 07:57 PM Response to Original message |

| 14. US to Implement "Temporary" Backstop to Money Market Funds (Updated) |

| Printer Friendly | Permalink | | Top |

| Demeter

|

Fri Sep-19-08 07:59 PM Response to Original message |

| 15. Why Have the Government Bailouts Involved Only a 79.9% Equity Position? by Adam Levitin |

| Printer Friendly | Permalink | | Top |

| Demeter

|

Fri Sep-19-08 08:39 PM Response to Reply #15 |

| 28. Henry Paulsons Frankenstein |

| Printer Friendly | Permalink | | Top |

| Demeter

|

Fri Sep-19-08 08:03 PM Response to Original message |

| 16. The Swedish banking crisis response - a model for the future? |

| Printer Friendly | Permalink | | Top |

| Demeter

|

Fri Sep-19-08 08:07 PM Response to Original message |

| 17. How Wall Street Lied to Its Computers By Saul Hansell |

| Printer Friendly | Permalink | | Top |

| Demeter

|

Fri Sep-19-08 08:10 PM Response to Original message |

| 18. Greenspans sins return to haunt us By David Blake |

| Printer Friendly | Permalink | | Top |

| Demeter

|

Fri Sep-19-08 08:14 PM Response to Original message |

| 20. How SEC Regulatory Exemptions Helped Lead to Collapse |

| Printer Friendly | Permalink | | Top |

| antigop

|

Sat Sep-20-08 10:19 AM Response to Reply #20 |

| 60. And Donaldson came in as SEC Chairman in 2003,right? |

| Printer Friendly | Permalink | | Top |

| antigop

|

Sat Sep-20-08 10:27 AM Response to Reply #60 |

| 61. Donaldson blamed focus on short-term earnings |

| Printer Friendly | Permalink | | Top |

| Demeter

|

Fri Sep-19-08 08:18 PM Response to Original message |

| 21. Bernanke: "We Have Lost Control" |

| Printer Friendly | Permalink | | Top |

| DemReadingDU

|

Fri Sep-19-08 08:22 PM Response to Original message |

| 22. You just bought yourself a country. Congratulations. |

| Printer Friendly | Permalink | | Top |

| Demeter

|

Fri Sep-19-08 08:28 PM Response to Reply #22 |

| 24. Perhaps, Having Bought It From the Pirates |

| Printer Friendly | Permalink | | Top |

| DemReadingDU

|

Fri Sep-19-08 08:33 PM Response to Reply #24 |

| 25. Click the links to see the pictures |

| Printer Friendly | Permalink | | Top |

| Demeter

|

Fri Sep-19-08 08:25 PM Response to Original message |

| 23. Why Wall Street is Melting Down, and What to Do About It |

| Printer Friendly | Permalink | | Top |

| Joe Chi Minh

|

Sat Sep-20-08 02:30 PM Response to Reply #23 |

| 74. You know, I thnk there's a hidden irony here. Is it my imagination, or didn't |

| Printer Friendly | Permalink | | Top |

| Demeter

|

Sat Sep-20-08 06:01 PM Response to Reply #74 |

| 82. It Was Greenspan's Bubble, But Yes, It Lasted Through Clinton's 2nd Term |

| Printer Friendly | Permalink | | Top |

| Joe Chi Minh

|

Sun Sep-21-08 07:55 AM Response to Reply #82 |

| 112. Thanks for the specifics. Another one, I dare say, like Bernanke, |

| Printer Friendly | Permalink | | Top |

| Demeter

|

Sun Sep-21-08 11:05 AM Response to Reply #112 |

| 128. Funny You Should Mention Driving a Car |

| Printer Friendly | Permalink | | Top |

| Joe Chi Minh

|

Sun Sep-21-08 11:31 AM Response to Reply #128 |

| 136. .... the icing on the cake. Good job Taleb's wit can give us some things |

| Printer Friendly | Permalink | | Top |

| Demeter

|

Fri Sep-19-08 08:33 PM Response to Original message |

| 26. Treasury Secretary Paulson leads us across the Rubicon |

| Printer Friendly | Permalink | | Top |

| Demeter

|

Fri Sep-19-08 08:36 PM Response to Original message |

| 27. National City gets approval to raise cash |

| Printer Friendly | Permalink | | Top |

| Demeter

|

Fri Sep-19-08 08:42 PM Response to Original message |

| 29. How many people have lost their jobs? |

| Printer Friendly | Permalink | | Top |

| Hugin

|

Fri Sep-19-08 08:55 PM Response to Original message |

| 30. Hello! |

| Printer Friendly | Permalink | | Top |

| Demeter

|

Fri Sep-19-08 09:43 PM Response to Reply #30 |

| 33. You What? |

| Printer Friendly | Permalink | | Top |

| Buttercup McToots

|

Sat Sep-20-08 06:31 AM Response to Reply #30 |

| 41. Where Prag? |

| Printer Friendly | Permalink | | Top |

| Hugin

|

Sat Sep-20-08 07:18 AM Response to Reply #41 |

| 48. Check this out. |

| Printer Friendly | Permalink | | Top |

| Demeter

|

Sun Sep-21-08 11:16 AM Response to Reply #48 |

| 130. Creepy and Insanely Hostile |

| Printer Friendly | Permalink | | Top |

| Demeter

|

Fri Sep-19-08 09:32 PM Response to Original message |

| 31. McCain May Not Understand the Fundamentals, But His Lobbyist Advisors Do |

| Printer Friendly | Permalink | | Top |

| Demeter

|

Fri Sep-19-08 09:41 PM Response to Original message |

| 32. It's the War, Stupid |

| Printer Friendly | Permalink | | Top |

| Demeter

|

Fri Sep-19-08 10:18 PM Response to Original message |

| 34. Dave Lindorff: You Can't Feel Blue About the Economy If You Want To. There Are No Blue Chips Anymore |

| Printer Friendly | Permalink | | Top |

| Demeter

|

Fri Sep-19-08 10:35 PM Response to Original message |

| 36. Here's What Happened Wednesday! |

| Printer Friendly | Permalink | | Top |

| Hugin

|

Sat Sep-20-08 06:35 AM Response to Reply #36 |

| 43. January 1940, eh? |

| Printer Friendly | Permalink | | Top |

| Demeter

|

Fri Sep-19-08 10:41 PM Response to Original message |

| 37. New Studies Report Wide Disparity in Health Care Plans By Perry Bacon Jr. |

| Printer Friendly | Permalink | | Top |

| Demeter

|

Fri Sep-19-08 10:43 PM Response to Original message |

| 38. That's It for Tonight, Folks--Sweet Dreams! |

| Printer Friendly | Permalink | | Top |

| Dr.Phool

|

Sat Sep-20-08 12:12 AM Response to Original message |

| 39. Kick! |

| Printer Friendly | Permalink | | Top |

| Buttercup McToots

|

Sat Sep-20-08 06:27 AM Response to Original message |

| 40. Good Mornin` |

| Printer Friendly | Permalink | | Top |

| Demeter

|

Sat Sep-20-08 11:44 AM Response to Reply #40 |

| 64. Good Thing It's Only Once a Year |

| Printer Friendly | Permalink | | Top |

| Buttercup McToots

|

Sat Sep-20-08 06:34 AM Response to Original message |

| 42. Resolution Trust: the mother of all scams |

| Printer Friendly | Permalink | | Top |

| Buttercup McToots

|

Sat Sep-20-08 06:36 AM Response to Reply #42 |

| 44. They want this thru fast...very fast...I scared I tell you... |

| Printer Friendly | Permalink | | Top |

| Hugin

|

Sat Sep-20-08 07:52 AM Response to Reply #44 |

| 51. What's that expression? Bum's Rush? |

| Printer Friendly | Permalink | | Top |

| Hugin

|

Sat Sep-20-08 07:54 AM Response to Reply #51 |

| 52. No, a 'bums rush' is what we need to do to Paulson, Bernake, and many others... |

| Printer Friendly | Permalink | | Top |

| Hugin

|

Sun Sep-21-08 02:23 AM Response to Reply #52 |

| 94. Railroaded! |

| Printer Friendly | Permalink | | Top |

| Karenina

|

Sat Sep-20-08 07:00 AM Response to Reply #42 |

| 46. Great graphic there! |

| Printer Friendly | Permalink | | Top |

| Demeter

|

Sat Sep-20-08 11:48 AM Response to Reply #42 |

| 65. Bernanke and Hank Did a Masterful Sell Job |

| Printer Friendly | Permalink | | Top |

| Buttercup McToots

|

Sat Sep-20-08 06:44 AM Response to Original message |

| 45. Bloomberg: Timing of taxpayer *ss-reaming |

| Printer Friendly | Permalink | | Top |

| Hugin

|

Sat Sep-20-08 07:57 AM Response to Reply #45 |

| 53. Is that seriously the headline? |

| Printer Friendly | Permalink | | Top |

| Demeter

|

Sat Sep-20-08 11:51 AM Response to Reply #45 |

| 66. Thing Is, They're Buying the Derivatives, Not the Actual Mortgages |

| Printer Friendly | Permalink | | Top |

| fedsron2us

|

Sun Sep-21-08 04:08 PM Response to Reply #66 |

| 145. Dervivatives and leverage are the root cause of this disaster |

| Printer Friendly | Permalink | | Top |

| Demeter

|

Sun Sep-21-08 05:41 PM Response to Reply #145 |

| 146. Exactly! Thanks for the link! |

| Printer Friendly | Permalink | | Top |

| Tansy_Gold

|

Sun Sep-21-08 08:52 PM Response to Reply #145 |

| 150. I posted this article as a new thread topic |

| Printer Friendly | Permalink | | Top |

| phrigndumass

|

Sat Sep-20-08 07:09 AM Response to Original message |

| 47. Rec'ing while I can, with a promise to come back Sunday morning to read :) |

| Printer Friendly | Permalink | | Top |

| UpInArms

|

Sat Sep-20-08 07:30 AM Response to Original message |

| 49. This one is must read! Morgan Stanley, Goldman love shorts...and hate them |

| Printer Friendly | Permalink | | Top |

| Hugin

|

Sat Sep-20-08 08:02 AM Response to Reply #49 |

| 54. Double standard? No wonder they act so schizoid. |

| Printer Friendly | Permalink | | Top |

| UpInArms

|

Sat Sep-20-08 07:39 AM Response to Original message |

| 50. How AIG fell apart - good explanation of why we need to stick a fork in CDSs |

| Printer Friendly | Permalink | | Top |

| Tansy_Gold

|

Sun Sep-21-08 07:13 AM Response to Reply #50 |

| 106. This is certainly not unexpected, is it???? |

| Printer Friendly | Permalink | | Top |

| Buttercup McToots

|

Sat Sep-20-08 08:25 AM Response to Original message |

| 55. From Mike Morgan "Move Money to Money Markets Now " |

| Printer Friendly | Permalink | | Top |

| Tansy_Gold

|

Sun Sep-21-08 07:14 AM Response to Reply #55 |

| 107. What money? n/t |

| Printer Friendly | Permalink | | Top |

| Mojorabbit

|

Sun Sep-21-08 10:59 PM Response to Reply #55 |

| 154. Too late |

| Printer Friendly | Permalink | | Top |

| Buttercup McToots

|

Sat Sep-20-08 08:35 AM Response to Original message |

| 56. Proposals for US Bad-Debt Fund Begin to Emerge |

| Printer Friendly | Permalink | | Top |

| antigop

|

Sat Sep-20-08 10:12 AM Response to Reply #56 |

| 58. ..contention in Congress over whether to cede equity |

| Printer Friendly | Permalink | | Top |

| antigop

|

Sat Sep-20-08 10:13 AM Response to Reply #56 |

| 59. Anyone want to bet that retroactive immunity will be thrown in,too? n/t |

| Printer Friendly | Permalink | | Top |

| Roland99

|

Sat Sep-20-08 09:34 AM Response to Original message |

| 57. Is this a bottle in front of me or a frontal lobotomy? |

| Printer Friendly | Permalink | | Top |

| antigop

|

Sat Sep-20-08 10:35 AM Response to Original message |

| 62. "The proposal does not specify what the government would get in return from financial companies" |

| Printer Friendly | Permalink | | Top |

| antigop

|

Sat Sep-20-08 10:39 AM Response to Original message |

| 63. WSJ: As Times Turn Tough, New York's wealthy economize |

| Printer Friendly | Permalink | | Top |

| Pale Blue Dot

|

Sat Sep-20-08 01:08 PM Response to Original message |

| 67. I'll ask the "real" smartest people in the room: How much time do you think the Fed bought? |

| Printer Friendly | Permalink | | Top |

| Karenina

|

Sat Sep-20-08 01:47 PM Response to Reply #67 |

| 69. Cassandra calling 20 October! |

| Printer Friendly | Permalink | | Top |

| DemReadingDU

|

Sat Sep-20-08 01:52 PM Response to Reply #67 |

| 70. It seems like a Naomi Klein Shock Doctrine |

| Printer Friendly | Permalink | | Top |

| Dr.Phool

|

Sat Sep-20-08 02:32 PM Response to Reply #70 |

| 75. We need a general strike. |

| Printer Friendly | Permalink | | Top |

| DemReadingDU

|

Sat Sep-20-08 03:03 PM Response to Reply #75 |

| 78. yeh, general strike, shut down everything |

| Printer Friendly | Permalink | | Top |

| Dr.Phool

|

Sat Sep-20-08 02:29 PM Response to Reply #67 |

| 73. I'm no expert, but I'd say days. |

| Printer Friendly | Permalink | | Top |

| Demeter

|

Sat Sep-20-08 06:08 PM Response to Reply #67 |

| 83. A Few Days, Maybe |

| Printer Friendly | Permalink | | Top |

| Hugin

|

Sat Sep-20-08 07:16 PM Response to Reply #67 |

| 85. Considering there's no way they could implement it before next year... |

| Printer Friendly | Permalink | | Top |

| Demeter

|

Sat Sep-20-08 07:19 PM Response to Reply #85 |

| 86. Paulson Can Really Move When He Wants To--Don't Be too Sure |

| Printer Friendly | Permalink | | Top |

| Dr.Phool

|

Sat Sep-20-08 10:01 PM Response to Reply #86 |

| 89. Bush-Cheney, Poulson-Bernanke are talking to the same gullible audience. |

| Printer Friendly | Permalink | | Top |

| Waiting For Everyman

|

Sat Sep-20-08 11:49 PM Response to Reply #89 |

| 91. You're right. |

| Printer Friendly | Permalink | | Top |

| Hugin

|

Sun Sep-21-08 02:09 AM Response to Reply #91 |

| 93. Sound thinking. |

| Printer Friendly | Permalink | | Top |

| Hugin

|

Sun Sep-21-08 02:05 AM Response to Reply #89 |

| 92. No! Wait! Stop! Don't! There, I said it so their Mother didn't have to... |

| Printer Friendly | Permalink | | Top |

| DemReadingDU

|

Sat Sep-20-08 01:37 PM Response to Original message |

| 68. William Greider: Paulson Bailout Plan a Historic Swindle |

| Printer Friendly | Permalink | | Top |

| Ghost Dog

|

Sun Sep-21-08 02:49 AM Response to Reply #68 |

| 97. Further to that: The Mother of All Frauds (Denninger): |

| Printer Friendly | Permalink | | Top |

| DemReadingDU

|

Sun Sep-21-08 06:52 AM Response to Reply #97 |

| 103. Thanks, Denniger lays it all out. |

| Printer Friendly | Permalink | | Top |

| Dr.Phool

|

Sat Sep-20-08 02:18 PM Response to Original message |

| 72. Kevin Phillips on Moyers last night. |

| Printer Friendly | Permalink | | Top |

| Karenina

|

Sat Sep-20-08 04:24 PM Response to Reply #72 |

| 80. Great interview! |

| Printer Friendly | Permalink | | Top |

| Demeter

|

Sat Sep-20-08 07:25 PM Response to Reply #80 |

| 88. Agreed! And VERY Depressing |

| Printer Friendly | Permalink | | Top |

| Pale Blue Dot

|

Sat Sep-20-08 10:19 PM Response to Reply #88 |

| 90. I think you're deluding yourself (but I hope I'm wrong) |

| Printer Friendly | Permalink | | Top |

| Tansy_Gold

|

Sun Sep-21-08 07:24 AM Response to Reply #90 |

| 108. I dunno. My brain is working in strange directions after four |

| Printer Friendly | Permalink | | Top |

| Demeter

|

Sun Sep-21-08 11:24 AM Response to Reply #90 |

| 131. Sometimes, Times Make the Man or Woman |

| Printer Friendly | Permalink | | Top |

| ozymandius

|

Sat Sep-20-08 04:04 PM Response to Original message |

| 79. What in the Hell just happened? |

| Printer Friendly | Permalink | | Top |

| lostnotforgotten

|

Sun Sep-21-08 06:49 AM Response to Reply #79 |

| 102. Debt - 596 Trillion Derivatives - 58 Trillion Credit Default Swaps - 2.5 Trillion Credit Card |

| Printer Friendly | Permalink | | Top |

| Demeter

|

Sat Sep-20-08 07:22 PM Response to Original message |

| 87. "First Toxic Bank"; BBC Business Editor on the bailout |

| Printer Friendly | Permalink | | Top |

| Karenina

|

Sun Sep-21-08 05:09 AM Response to Reply #87 |

| 99. Fix for your link: |

| Printer Friendly | Permalink | | Top |

| Hugin

|

Sun Sep-21-08 04:09 AM Response to Original message |

| 98. Here's what should happen, but, won't... |

| Printer Friendly | Permalink | | Top |

| Dr.Phool

|

Sun Sep-21-08 07:43 AM Response to Reply #98 |

| 111. A sick mind is a terrible thing to waste, isn't it? |

| Printer Friendly | Permalink | | Top |

| Hugin

|

Sun Sep-21-08 08:54 AM Response to Reply #111 |

| 116. Good term.... 'deliberative pause'. |

| Printer Friendly | Permalink | | Top |

| Demeter

|

Sun Sep-21-08 11:27 AM Response to Reply #116 |

| 132. Love That Term: Banana Republican! |

| Printer Friendly | Permalink | | Top |

| ozymandius

|

Sun Sep-21-08 06:09 AM Response to Original message |

| 100. Stop the mother-of-all-muggings before it starts. |

| Printer Friendly | Permalink | | Top |

| DemReadingDU

|

Sun Sep-21-08 06:49 AM Response to Reply #100 |

| 101. Thanks, I am stunned. speechless |

| Printer Friendly | Permalink | | Top |

| Buttercup McToots

|

Sun Sep-21-08 07:40 AM Response to Reply #101 |

| 110. I don't feel go either, Dem |

| Printer Friendly | Permalink | | Top |

| UpInArms

|

Sun Sep-21-08 11:05 AM Response to Reply #100 |

| 127. according to this chart, a banana has more worth |

| Printer Friendly | Permalink | | Top |

| Demeter

|

Sun Sep-21-08 11:30 AM Response to Reply #127 |

| 135. Where did you get that graph? |

| Printer Friendly | Permalink | | Top |

| UpInArms

|

Sun Sep-21-08 02:26 PM Response to Reply #135 |

| 143. from Ozy's post #100 |

| Printer Friendly | Permalink | | Top |

| Roland99

|

Sun Sep-21-08 07:34 AM Response to Original message |

| 109. New Debt Ceiling: $11.3 Trillion.... $$$11.3 TRILLION$$$ (Nearly double its 2001 level) |

| Printer Friendly | Permalink | | Top |

| Roland99

|

Sun Sep-21-08 07:56 AM Response to Original message |

| 113. Is the proposed bailout legislation even Constitutional??? |

| Printer Friendly | Permalink | | Top |

| DemReadingDU

|

Sun Sep-21-08 08:05 AM Response to Original message |

| 114. Mike Whitney: Grasping at Straws |

| Printer Friendly | Permalink | | Top |

| Tansy_Gold

|

Sun Sep-21-08 09:03 AM Response to Reply #114 |

| 118. no shit, sherlock. |

| Printer Friendly | Permalink | | Top |

| Demeter

|

Sun Sep-21-08 11:31 AM Response to Reply #114 |

| 137. Great And Unfortunately True Analogy |

| Printer Friendly | Permalink | | Top |

| antigop

|

Sun Sep-21-08 08:46 AM Response to Original message |

| 115. Some thoughts after another restless night.... |

| Printer Friendly | Permalink | | Top |

| DemReadingDU

|

Sun Sep-21-08 09:15 AM Response to Reply #115 |

| 121. My previous life |

| Printer Friendly | Permalink | | Top |

| antigop

|

Sun Sep-21-08 08:58 AM Response to Original message |

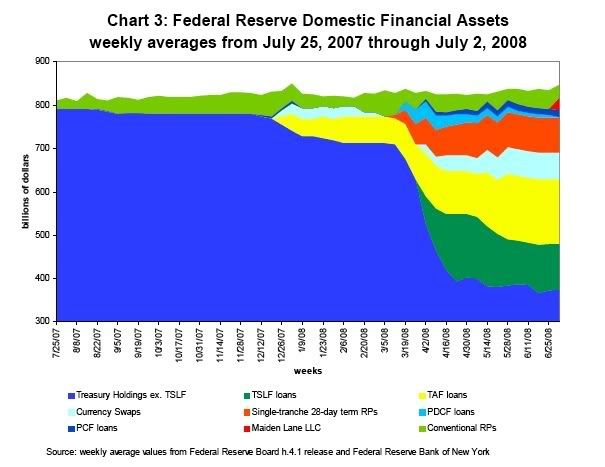

| 117. The Fed, now with more junk |

| Printer Friendly | Permalink | | Top |

| Demeter

|

Sun Sep-21-08 11:34 AM Response to Reply #117 |

| 138. That's One Way to Put the Fed Out of Business! |

| Printer Friendly | Permalink | | Top |

| Pale Blue Dot

|

Sun Sep-21-08 09:20 AM Response to Original message |

| 122. Paulson resists calls for added help in bailout |

| Printer Friendly | Permalink | | Top |

| Hugin

|

Sun Sep-21-08 09:25 AM Response to Reply #122 |

| 124. Seeing as they already blew the 'clean' part by playing dirty... |

| Printer Friendly | Permalink | | Top |

| Demeter

|

Sun Sep-21-08 11:35 AM Response to Reply #122 |

| 139. "Clean and Quick", Eh? Why Does Assassination Spring to My Mind? |

| Printer Friendly | Permalink | | Top |

| Pale Blue Dot

|

Sun Sep-21-08 09:21 AM Response to Original message |

| 123. Paulson says foreign banks can use U.S. rescue plan |

| Printer Friendly | Permalink | | Top |

| Hugin

|

Sun Sep-21-08 09:29 AM Response to Reply #123 |

| 125. Oh, great... Now we've become cesspit-to-the-world. |

| Printer Friendly | Permalink | | Top |

| Dr.Phool

|

Sun Sep-21-08 11:28 AM Response to Original message |

| 133. Brazen Political Advertisement! |

| Printer Friendly | Permalink | | Top |

| Demeter

|

Sun Sep-21-08 11:37 AM Response to Reply #133 |

| 140. Hearing No Objections, Consider It Acceptable! |

| Printer Friendly | Permalink | | Top |

| DemReadingDU

|

Sun Sep-21-08 11:29 AM Response to Original message |

| 134. Chris Martenson: What the latest bailout plan means |

| Printer Friendly | Permalink | | Top |

| Demeter

|

Sun Sep-21-08 12:03 PM Response to Original message |

| 141. Well, Folks: I'm Quitting Early This Weekend |

| Printer Friendly | Permalink | | Top |

| Demeter

|

Sun Sep-21-08 12:09 PM Response to Original message |

| 142. Go See This Link! |

| Printer Friendly | Permalink | | Top |

| DemReadingDU

|

Sun Sep-21-08 03:25 PM Response to Original message |

| 144. more from ilargi at The Automatic Earth |

| Printer Friendly | Permalink | | Top |

| UpInArms

|

Sun Sep-21-08 06:45 PM Response to Original message |

| 147. Monday Morning Futures: Dow down 201 points at 7:10 p.m. EST Sunday |

| Printer Friendly | Permalink | | Top |

| antigop

|

Sun Sep-21-08 07:44 PM Response to Original message |

| 148. The shadow banking system is unravelling |

| Printer Friendly | Permalink | | Top |

| antigop

|

Sun Sep-21-08 08:35 PM Response to Original message |

| 149. Anyone have any idea how they arrived at a $700 billion figure? |

| Printer Friendly | Permalink | | Top |

| DemReadingDU

|

Sun Sep-21-08 10:19 PM Response to Reply #149 |

| 151. good question, curious |

| Printer Friendly | Permalink | | Top |

| antigop

|

Sun Sep-21-08 10:30 PM Response to Reply #151 |

| 152. I thought it might be the size of the Social Security Trust fund-- but I checked |

| Printer Friendly | Permalink | | Top |

| antigop

|

Sun Sep-21-08 10:37 PM Response to Original message |

| 153. Federal Reserve changes status of Goldman Sachs and Morgan Stanley to bank holding companies |

| Printer Friendly | Permalink | | Top |

| DU

AdBot (1000+ posts) |

Thu Apr 25th 2024, 11:45 AM Response to Original message |

| Advertisements [?] |

| Top |

| Home » Discuss » Editorials & Other Articles |

|

Powered by DCForum+ Version 1.1 Copyright 1997-2002 DCScripts.com

Software has been extensively modified by the DU administrators

Important Notices: By participating on this discussion board, visitors agree to abide by the rules outlined on our Rules page. Messages posted on the Democratic Underground Discussion Forums are the opinions of the individuals who post them, and do not necessarily represent the opinions of Democratic Underground, LLC.

Home | Discussion Forums | Journals | Store | Donate

About DU | Contact Us | Privacy Policy

Got a message for Democratic Underground? Click here to send us a message.

© 2001 - 2011 Democratic Underground, LLC