http://www.huffingtonpost.com/2009/02/19/alan-greenspan-the-oracle_n_168168.htmlOn June 10, 1999, at the height of his power, Alan Greenspan told members of Harvard's graduating class how, in the future, they should assess their lives: "The true measure of a career is to be able to be content, even proud, that you succeeded through your own endeavors without leaving a trail of casualties in your wake."

At the time, Greenspan, 73, clearly thought he had lived up to his own standard. Four months earlier, on February 15, Time magazine had honored him with a cover story, presenting Greenspan as the de facto chair of the three-member "Committee To Save The World."

The American economy Greenspan had overseen for 12 years from his perch as chairman of the Federal Reserve was, by his description, "in the grip of what . . . Joseph Schumpeter, many years ago called 'creative destruction'.... This is the process by which wealth is created, incremental step by incremental step. It presupposes a continuous churning of an economy as the new displaces the old."

The free market, Greenspan told the graduating seniors, is a pillar of civilization which "presupposes the productive interaction of people engaged in the division of labor, driven -- I cannot resist the jargon -- by economic comparative advantage. This implies mutual exchange to mutual advantage among free people."

Greenspan's years of running the Federal Reserve, from August 1987 to January 2006, were a time of economic glory. On July 16, 2003, for example, when such other figures as Warren Buffett and George Soros were warning of the dangers of derivatives, Greenspan told the Senate Banking Committee, according to a transcript of the session:

"What we have found over the years in the marketplace is that derivatives have been an extraordinarily useful vehicle to transfer risk from those who shouldn't be taking it to those who are willing to and are capable of doing so. Prior to the advent of derivatives on a large scale, we did not have that capability. And we often had, for example, financial institutions, like banks, taking on undue risk and running into real, serious problems....

"The vast increase in the size of the over-the-counter derivatives markets is the result of the market finding them a very useful vehicle. And the question is, should these be regulated? Well, indeed, for the United States, they are obviously regulated to the extent that banks, being the crucial creators of these derivatives, are regulated by the banking agencies, but not beyond that. And the reason why we think it would be a mistake to go beyond that degree of regulation is that these derivative transactions are transactions amongst professionals. And the institutions which are involved have very considerable what we call counterparty surveillance, where, for example, one major bank will know far more about its customer, whether it's a bank or something else, than we could conceivably know as regulators. In a sense, this counterparty surveillance has become the crucial element which has created stability in that particular system."

Greenspan's tenure coincided with a period during which total wealth increased dramatically, although much of the growth was concentrated among the richest of the rich, not just the top one percent of the income distribution, but the top 0.1 percent.

The gross national product, in inflation-adjusted 2000 dollars, rose from $6.47 trillion in 1987 to $11.32 trillion in 2006, while unemployment fell by a substantial 1.6 percentage points, from 6.2 percent in 1987 to 4.6 percent in 2006. Corporate profits rose from $368.8 billion to $1.59 trillion, without adjusting for inflation.

Story continues below

The Dow Jones, which was just above 2700 when Greenspan took office in 1987, rose to over 11,000 in January, 2006, when he retired.

In one of his more controversial decisions, the Fed under Greenspan flooded the market with cash in the immediate aftermath of the 9/11 terrorist attacks and sharply cut interest rates as part of a worldwide effort on the part of central bankers to reinvigorate the global economy.

Now, three years after he left the Fed, Greenspan confronts a catastrophic legacy. All around him is the evidence of an extraordinary "trail of casualties" left in his wake -- men and women losing their jobs at a rate of half a million-a-month; foreclosures forcing Americans out of their homes; and the Dow plunged by 46.7 percent from its high of 14,164.53 on October 9, 2007.

The gross domestic product began to fall at an annual rate of 0.5 percent in the third quarter of 2008 and then accelerated to a 3.8 percent rate of decline in the fourth quarter; corporate profits fell by $160 billion from $1.67 trillion in the third quarter of 2007 to $1.51 trillion in the fourth quarter of 2008. The unemployment rate has risen from 4.7 percent in January 2006, when Greenspan retired, to 7.6 percent last month.

The Dow Jones Industrial Average, which reached a high of 14164.53 on October 9, 2007, has collapsed to 7,555.63 at the close of business Wednesday - a drop of nearly 47 percent.

Much of the blame has been aimed at Greenspan: "Because the Federal Reserve under Alan Greenspan pushed interest rates too low and kept them low for too long, and because regulation of financial intermediaries had over the years dwindled and became especially lax during the Bush Administration, the bankers were allowed, and competition forced them, to take risks that could have and have had disastrous results," wrote Richard A. Posner, Seventh Circuit Court of Appeals Judge.

Nobel Laureate Joseph Stiglitz adds other culprits as crucial to the making of the current economic crisis. Among them:

1) the April 1998, decision of President Clinton's Working Group on Financial Markets to quash a proposal by Brooksley E. Born, head of the Commodity Futures Trading Commission, to regulate derivatives;

2) enactment of Gramm-Leach-Bliley Act on November 12, 1999 allowing consolidation of commercial and investment banks;

3) passage of the Commodity Futures Modernization Act of 2000 removing derivatives from federal oversight;

4) the Bush tax cuts of 2001 and 2003;

5) the failure of the Federal Reserve to take responsibility for regulating derivatives; and

6) the Securities and Exchange Commission decision in April, 2004, to allow large investment banks to increase their debt-to-capital ratio from 12 to 1 to 30 to 1, or higher.

What each of these actions (and inactions) has in common is that Greenspan either initiated or endorsed them.

The rejection of Commodity Futures Trading Commission chief Born's proposal to regulate derivatives was backed by Treasury Secretary Robert E. Rubin and Securities and Exchange Commission Chairman Arthur Levitt Jr., both members of the Working Group on Financial Markets, but, according to most accounts, Greenspan led the charge.

Some argue that Greenspan was less an independent power in his own right than a reflection of the forces that have generally dominated the setting of banking regulation over the years.

Columbia economist Massimo Morelli, for example, contends that:

"allowing banks to become much more than banks and allowing investment banks to operate in an almost lawless environment were huge mistakes, and with large unfair distribution consequences....the strong financial lobbies have certainly had an impact on such mistakes, and so part of the responsibility goes certainly to the fed and treasury secretaries, but it would be hard for me to take sides on who or what institution was primarily responsible. The unfortunate point I would make today is that the same lobbies seem to be still very powerful, given the unfair distributional consequences of the TARP and the unwillingness of the decision makers in Washington to resolve the lending problems of this economy by a simple resort to swapping debt into equity, making the bank debt holders suffer to a greater extent than taxpayers."

Greenspan has struggled to come to terms with the economic collapse and his role in it.

Last autumn, with the economy in a tailspin, Greenspan remained remarkably sanguine, voicing little or no self-reproach for the possible consequences of his hands-off, free-market approach to the regulation of derivatives. In an October 2, 2008, speech at the Sandra Day O'Connor Conference at Georgetown University, Greenspan blamed a lack of trust, not a lack of regulation, for the financial meltdown, and predicted a quick turnaround (italics added):

"In a market system based on trust, reputation has a significant economic value. I am therefore distressed at how far we have let concerns for reputation slip in recent years. Reputation and the trust it fosters have always appeared to me to be the core attributes required of competitive markets. Laws at best can prescribe only a small fraction of the day-by-day activities in the marketplace. When trust is lost, a nation's ability to transact business is palpably undermined. In the marketplace, uncertainties created by not always truthful counterparties raise credit risk and thereby increase real interest rates and weaker economies.

"During the past year, lack of trust in the validity of accounting records of banks and other financial institutions in the context of inadequate capital led to a massive hesitancy in lending to them. The result has been a freezing up of credit. As I noted in my opening remarks, trust will eventually reemerge as investors dip hesitantly back into the marketplace. From that point, history tells us, financial and economic revival sets in. I suspect it will be sooner rather than later. In either event, human nature being what it is, revival will come. It always has in this society governed by that remarkable document we call the Constitution of the United States."

Just 21 days later, however, testifying before the House Oversight and Reform Committee on October 23, 2008, a suddenly chastened Greenspan appeared repentant and certainly no longer the defender of untrammeled laissez-faire.

In his prepared testimony, Greenspan told the committee:

"

hose of us who have looked to the self-interest of lending institutions to protect shareholder's equity (myself especially) are in a state of shocked disbelief. Such counterparty surveillance is a central pillar of our financial markets' state of balance."

Under questioning by committee chair Henry Waxman, Greenspan was more explicit:

"Waxman: his is your statement. 'I do have an ideology. My judgment is that free competitive markets are by far the unrivaled way to organize economies. We've tried regulation. None meaningfully worked.'....Do you feel that your ideology pushed you to make decisions that you wish you had not made?

"Greenspan: Well, remember that what an ideology is. It's a conceptual framework with the way people deal with reality. Everyone has one. You have to. To exist you need an ideology. The question is whether it is accurate or not. And what I'm saying to you is 'yes, I have found a flaw.' I don't know how significant or permanent it is. But I have been very distressed by that fact.....A flaw in the model that I perceived is the critical functioning structure that defines how the world works, so to speak."

More recently, Greenspan had adopted a different tack. Once proud of his nickname, "The Oracle," and of his de facto chairmanship of the Committee to Save the World, Greenspan told CNBC that during the critical years leading up to the 2008 collapse, he was both ignorant of the scope of the problem and powerless to deal with it. An account of the CNBC program, first aired on February 12, 2009, reads:

"I remember my initial response when a staff member came up to me and he says, 'I don't know if you have seen something like this'," while showing the then-Fed chairman data that subprime mortgages represented 20 percent of all new mortgages. "I said, 'I don't believe that number,'" Greenspan recounted.

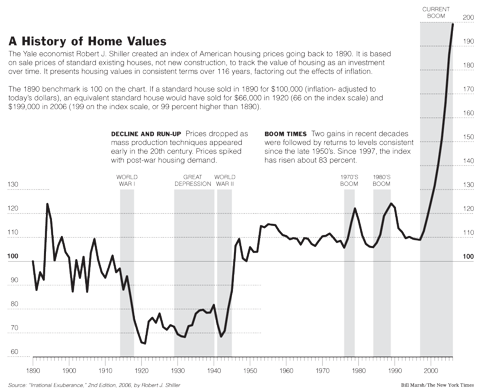

Asked if the Fed could have prevented the housing bubble, Greenspan pleaded powerlessness: "If we tried to suppress the expansion of the subprime market, do you think that would have gone over very well with the Congress?...When it looked as though we were dealing with a major increase in home ownership, which is of unquestioned value to this society -- would we have been able to do that? I doubt it."

Not only that, Greenspan contended on CNBC, but if the Fed had taken action, the results would have been disastrous: "We could have basically clamped down on the American economy, generated a 10 percent unemployment rate. And I will guarantee we would not have had a housing boom, stock market boom, or indeed a particularly good economy either."

Most recently, Greenspan's ideological journey has taken an abrupt left turn. On February 18, the Financial Times reported that the one-time libertarian devotee of Ayn Rand now thinks the government might be best advised to take over 'lemon' banks. "It may be necessary to temporarily nationalize some banks in order to facilitate a swift and orderly restructuring," he said in an interview.

Now, there is no way to predict what the former Chairman will say in his next commencement address.