| Latest | Greatest | Lobby | Journals | Search | Options | Help | Login |

|

|

|

This topic is archived. |

| Home » Discuss » Editorials & Other Articles |

|

| Demeter

|

Fri Sep-25-09 04:38 PM Original message |

| Weekend Economists Lost Weekend September 25-27, 2009 |

| Printer Friendly | Permalink | | Top |

| Demeter

|

Fri Sep-25-09 04:41 PM Response to Original message |

| 1. Oliphant on Obama and Racism--Another Innocence Lost |

| Printer Friendly | Permalink | | Top |

| Demeter

|

Fri Sep-25-09 04:46 PM Response to Original message |

| 2. And to Start Off Another Bank Fails in Georgia |

| Printer Friendly | Permalink | | Top |

| Demeter

|

Fri Sep-25-09 04:48 PM Response to Reply #2 |

| 3. Lost Horizon - Share the Joy - Olivia Hussey |

| Printer Friendly | Permalink | | Top |

| Dr.Phool

|

Fri Sep-25-09 04:49 PM Response to Reply #2 |

| 4. Do they have any banks left in Georgia? |

| Printer Friendly | Permalink | | Top |

| Demeter

|

Fri Sep-25-09 05:09 PM Response to Reply #4 |

| 7. Why Ask Me? I thought You LIVED There! |

| Printer Friendly | Permalink | | Top |

| Dr.Phool

|

Fri Sep-25-09 05:36 PM Response to Reply #7 |

| 11. Nah, I'm in suburb of Georgia. |

| Printer Friendly | Permalink | | Top |

| Demeter

|

Fri Sep-25-09 06:05 PM Response to Reply #2 |

| 21. Midnight Raid to Georgia - Capitol Steps |

| Printer Friendly | Permalink | | Top |

| DemReadingDU

|

Fri Sep-25-09 06:26 PM Response to Reply #21 |

| 27. First time seeing these Capitol Steps videos |

| Printer Friendly | Permalink | | Top |

| Seldona

|

Fri Sep-25-09 06:51 PM Response to Reply #2 |

| 35. 'SO, OUT OF $2 BILLION ASSETS, HALF IS GARBAGE!' |

| Printer Friendly | Permalink | | Top |

| Po_d Mainiac

|

Sat Sep-26-09 08:22 AM Response to Reply #2 |

| 55. How can this be? |

| Printer Friendly | Permalink | | Top |

| DemReadingDU

|

Sat Sep-26-09 09:05 AM Response to Reply #2 |

| 56. only 1 bank this week? |

| Printer Friendly | Permalink | | Top |

| Demeter

|

Sat Sep-26-09 08:24 PM Response to Reply #56 |

| 59. It's A Rather Large Loss, Though |

| Printer Friendly | Permalink | | Top |

| Demeter

|

Fri Sep-25-09 05:07 PM Response to Original message |

| 5. German recovery loses momentum (that was short) |

| Printer Friendly | Permalink | | Top |

| Demeter

|

Fri Sep-25-09 05:08 PM Response to Reply #5 |

| 6. Kroes warns EU over stealing car jobs |

| Printer Friendly | Permalink | | Top |

| Demeter

|

Fri Sep-25-09 06:08 PM Response to Reply #6 |

| 22. Help Me Honda - Capitol Steps |

| Printer Friendly | Permalink | | Top |

| DemReadingDU

|

Fri Sep-25-09 06:29 PM Response to Reply #22 |

| 28. a different spin on bailouts |

| Printer Friendly | Permalink | | Top |

| Demeter

|

Fri Sep-25-09 05:11 PM Response to Original message |

| 8. Employment Oppty! Bullet Makers 'Working Overtime' in US |

| Printer Friendly | Permalink | | Top |

| Demeter

|

Fri Sep-25-09 05:12 PM Response to Reply #8 |

| 9. Pack The Knife - Capitol Steps |

| Printer Friendly | Permalink | | Top |

| DemReadingDU

|

Fri Sep-25-09 06:31 PM Response to Reply #9 |

| 29. Next time I fly |

| Printer Friendly | Permalink | | Top |

| Po_d Mainiac

|

Sat Sep-26-09 07:10 AM Response to Reply #29 |

| 53. Yup, u blend in with the masses that way n/t |

| Printer Friendly | Permalink | | Top |

| DemReadingDU

|

Fri Sep-25-09 05:26 PM Response to Original message |

| 10. Elephant in the Room |

| Printer Friendly | Permalink | | Top |

| Demeter

|

Fri Sep-25-09 05:51 PM Response to Reply #10 |

| 13. Ah, the English! Such a Contrast Between Manners and Humor |

| Printer Friendly | Permalink | | Top |

| Dr.Phool

|

Fri Sep-25-09 05:52 PM Response to Reply #10 |

| 14. "Debt is Dandy" .....Prick Muncher Gordon Brown. |

| Printer Friendly | Permalink | | Top |

| Demeter

|

Fri Sep-25-09 05:45 PM Response to Original message |

| 12. Fed eyes tie-up with mutual funds |

| Printer Friendly | Permalink | | Top |

| Demeter

|

Fri Sep-25-09 05:53 PM Response to Reply #12 |

| 15. Ain't No Surplus - Capitol Steps |

| Printer Friendly | Permalink | | Top |

| DemReadingDU

|

Fri Sep-25-09 06:33 PM Response to Reply #15 |

| 30. Ain't that the truth |

| Printer Friendly | Permalink | | Top |

| Demeter

|

Fri Sep-25-09 05:56 PM Response to Original message |

| 16. China rolls over $36bn of bail-out bonds |

| Printer Friendly | Permalink | | Top |

| Demeter

|

Fri Sep-25-09 06:03 PM Response to Reply #16 |

| 20. Credit Suisse bankers poised for pay-out |

| Printer Friendly | Permalink | | Top |

| Demeter

|

Fri Sep-25-09 06:37 PM Response to Reply #20 |

| 33. Lost Horizon 1973 - The World Is A Circle - Liv Ullman - Bobby Van |

| Printer Friendly | Permalink | | Top |

| Demeter

|

Fri Sep-25-09 05:58 PM Response to Original message |

| 17. BP given new warning over Texas refinery |

| Printer Friendly | Permalink | | Top |

| Demeter

|

Fri Sep-25-09 06:00 PM Response to Reply #17 |

| 18. Chevron takes Ecuador fight to the Hague |

| Printer Friendly | Permalink | | Top |

| Demeter

|

Fri Sep-25-09 06:01 PM Response to Reply #18 |

| 19. Capitol Steps - What Kind Of Fuel Am I |

| Printer Friendly | Permalink | | Top |

| DemReadingDU

|

Fri Sep-25-09 06:36 PM Response to Reply #19 |

| 32. What kind of cost is this? |

| Printer Friendly | Permalink | | Top |

| Demeter

|

Fri Sep-25-09 06:13 PM Response to Reply #18 |

| 25. God Bless My SUV - Capitol Steps |

| Printer Friendly | Permalink | | Top |

| DemReadingDU

|

Fri Sep-25-09 06:44 PM Response to Reply #25 |

| 34. only gets 5 MPG |

| Printer Friendly | Permalink | | Top |

| Demeter

|

Fri Sep-25-09 07:00 PM Response to Reply #34 |

| 38. Thanks! |

| Printer Friendly | Permalink | | Top |

| Demeter

|

Fri Sep-25-09 06:09 PM Response to Original message |

| 23. GIC makes $1.6bn from Citi stake sale |

| Printer Friendly | Permalink | | Top |

| Demeter

|

Fri Sep-25-09 06:12 PM Response to Original message |

| 24. Moodys warns over living wills |

| Printer Friendly | Permalink | | Top |

| Demeter

|

Fri Sep-25-09 06:21 PM Response to Original message |

| 26. Willis latest to leave low-tax Bermuda |

| Printer Friendly | Permalink | | Top |

| Demeter

|

Fri Sep-25-09 06:34 PM Response to Reply #26 |

| 31. Obama Mia! |

| Printer Friendly | Permalink | | Top |

| Demeter

|

Fri Sep-25-09 06:53 PM Response to Original message |

| 36. The End Of Capitalism: Ahmadinejad Speech at the UN |

| Printer Friendly | Permalink | | Top |

| Demeter

|

Fri Sep-25-09 06:55 PM Response to Reply #36 |

| 37. East Africa's drought A catastrophe is looming |

| Printer Friendly | Permalink | | Top |

| Demeter

|

Fri Sep-25-09 07:03 PM Response to Original message |

| 39. Time to Change Bernanke's Medication? Secret White House letter to G-20 By Greg Palast |

| Printer Friendly | Permalink | | Top |

| Demeter

|

Fri Sep-25-09 07:04 PM Response to Reply #39 |

| 40. Card Defaults Surge in August to 11.49%, Moodys Says (Update1) |

| Printer Friendly | Permalink | | Top |

| Demeter

|

Fri Sep-25-09 07:18 PM Response to Reply #40 |

| 41. Critics: TARP Has Failed to Halt Foreclosures or Job Losses |

| Printer Friendly | Permalink | | Top |

| Demeter

|

Fri Sep-25-09 07:19 PM Response to Reply #41 |

| 42. Lost Horizon- Reflections |

| Printer Friendly | Permalink | | Top |

| DemReadingDU

|

Fri Sep-25-09 07:26 PM Response to Reply #41 |

| 43. When do people understand that there won't be any recovery |

| Printer Friendly | Permalink | | Top |

| Hugin

|

Fri Sep-25-09 10:26 PM Response to Reply #41 |

| 46. But, then... Doing something about those things was never a part of TARP. |

| Printer Friendly | Permalink | | Top |

| DemReadingDU

|

Sat Sep-26-09 10:39 AM Response to Reply #41 |

| 57. Barofsky Sees a 'Far More Dangerous' Financial Situation |

| Printer Friendly | Permalink | | Top |

| Demeter

|

Fri Sep-25-09 07:33 PM Response to Original message |

| 44. The Economy Is A Lie, Too By Paul Craig Roberts |

| Printer Friendly | Permalink | | Top |

| Demeter

|

Fri Sep-25-09 07:38 PM Response to Reply #44 |

| 45. And Here I Come to a Natural Stopping Point |

| Printer Friendly | Permalink | | Top |

| hamerfan

|

Fri Sep-25-09 10:49 PM Response to Reply #45 |

| 47. K&R, n/t |

| Printer Friendly | Permalink | | Top |

| Demeter

|

Sat Sep-26-09 06:37 AM Response to Original message |

| 48. Banks fight to kill proposed consumer protection agency |

| Printer Friendly | Permalink | | Top |

| Demeter

|

Sat Sep-26-09 06:43 AM Response to Original message |

| 49. Just When You Thought It Couldn't Get Worse: Carlyle invests in Chinese milk powder maker |

| Printer Friendly | Permalink | | Top |

| Demeter

|

Sat Sep-26-09 06:45 AM Response to Original message |

| 50. California bond issue draws strong demand |

| Printer Friendly | Permalink | | Top |

| Demeter

|

Sat Sep-26-09 06:48 AM Response to Original message |

| 51. Business coalition urges pay overhaul (THE SKY IS FALLING! THE SKY IS FALLING!) |

| Printer Friendly | Permalink | | Top |

| Po_d Mainiac

|

Sat Sep-26-09 06:56 AM Response to Original message |

| 52. The Biggest Government Bailout Is Yet To Come |

| Printer Friendly | Permalink | | Top |

| Demeter

|

Sat Sep-26-09 07:53 AM Response to Original message |

| 54. Steve Keen: On the Edge with Max Keiser |

| Printer Friendly | Permalink | | Top |

| DemReadingDU

|

Sat Sep-26-09 07:21 PM Response to Original message |

| 58. NPR: Return to the Giant Pool of Money |

| Printer Friendly | Permalink | | Top |

| Demeter

|

Sat Sep-26-09 08:31 PM Response to Reply #58 |

| 60. Thanks DRDU! |

| Printer Friendly | Permalink | | Top |

| Demeter

|

Sun Sep-27-09 10:49 AM Response to Original message |

| 61. CEO of International Swaps & Derivatives Association says trust us |

| Printer Friendly | Permalink | | Top |

| Demeter

|

Sun Sep-27-09 10:54 AM Response to Original message |

| 62. Gross: The new normal for the next 10 years and maybe even the next 20 years |

| Printer Friendly | Permalink | | Top |

| Demeter

|

Sun Sep-27-09 10:56 AM Response to Original message |

| 63. The origin of the U.S. dollar as legal tender and its link to Depression |

| Printer Friendly | Permalink | | Top |

| Demeter

|

Sun Sep-27-09 10:58 AM Response to Original message |

| 64. The FDIC to get credit from banks even while banks restrict lending |

| Printer Friendly | Permalink | | Top |

| Demeter

|

Sun Sep-27-09 10:59 AM Response to Original message |

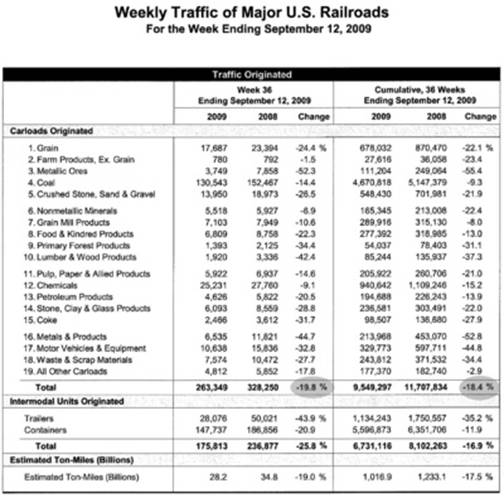

| 65. Railroad Traffic Decline Accelerates (Withering Green Shoot Watch) |

| Printer Friendly | Permalink | | Top |

| Demeter

|

Sun Sep-27-09 11:02 AM Response to Original message |

| 66. Deflation? By George Washington of Washingtons Blog. |

| Printer Friendly | Permalink | | Top |

| Demeter

|

Sun Sep-27-09 11:03 AM Response to Original message |

| 67. William K. Blacks Proposal for Systemically Dangerous Institutions |

| Printer Friendly | Permalink | | Top |

| Demeter

|

Sun Sep-27-09 11:04 AM Response to Original message |

| 68. Do Ben and Tim = Thelma and Louise? |

| Printer Friendly | Permalink | | Top |

| Demeter

|

Sun Sep-27-09 06:32 PM Response to Original message |

| 69. That's All Folks! |

| Printer Friendly | Permalink | | Top |

| DU

AdBot (1000+ posts) |

Thu Apr 25th 2024, 06:27 AM Response to Original message |

| Advertisements [?] |

| Top |

| Home » Discuss » Editorials & Other Articles |

|

Powered by DCForum+ Version 1.1 Copyright 1997-2002 DCScripts.com

Software has been extensively modified by the DU administrators

Important Notices: By participating on this discussion board, visitors agree to abide by the rules outlined on our Rules page. Messages posted on the Democratic Underground Discussion Forums are the opinions of the individuals who post them, and do not necessarily represent the opinions of Democratic Underground, LLC.

Home | Discussion Forums | Journals | Store | Donate

About DU | Contact Us | Privacy Policy

Got a message for Democratic Underground? Click here to send us a message.

© 2001 - 2011 Democratic Underground, LLC

?bgcolor=%23B3CDE7&chart_type=line&drp=0&graph_bgcolor=%23FFFFFF&height=480&preserve_ratio=checked&recession_bars=On&txtcolor=%23000000&width=800&id=EXCRESNS&transformation=lin&scale=Left&range=Custom&cosd=1989-01-01&coed=2009-07-01&line_color=%230000FF&vintage_date=2009-08-27&line_style=Solid&mark_type=NONE&mma=0

?bgcolor=%23B3CDE7&chart_type=line&drp=0&graph_bgcolor=%23FFFFFF&height=480&preserve_ratio=checked&recession_bars=On&txtcolor=%23000000&width=800&id=EXCRESNS&transformation=lin&scale=Left&range=Custom&cosd=1989-01-01&coed=2009-07-01&line_color=%230000FF&vintage_date=2009-08-27&line_style=Solid&mark_type=NONE&mma=0