From the article, "The U.S. is up in arms, so to speak, because private American firms can't take on such riskbut their French, Russian and other state-backed competitors can."

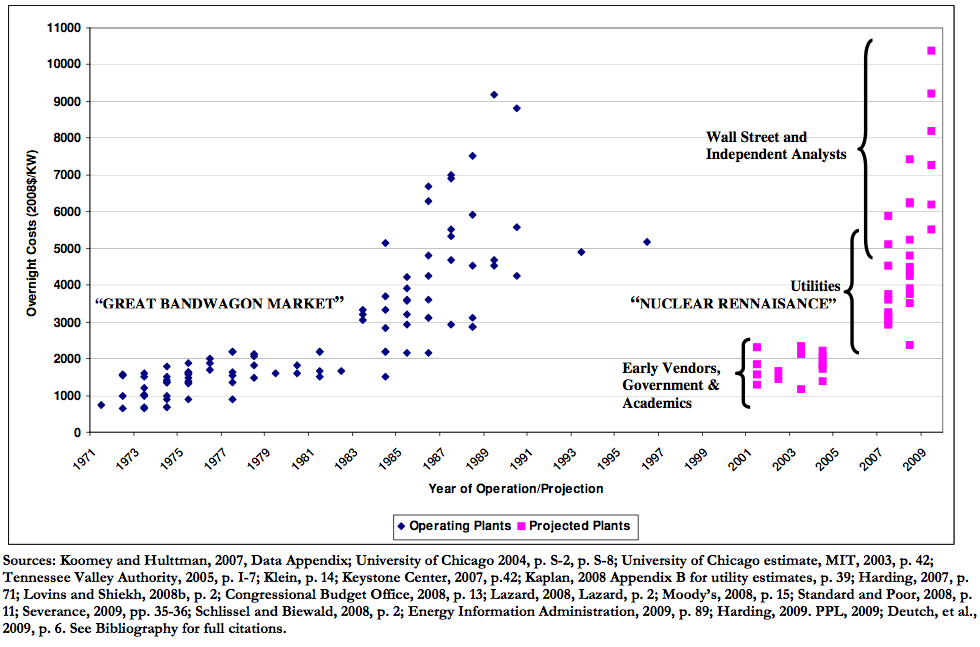

The problem is simple. Nuclear power projects have a very, very long payback time for investors because of the scale of the projects; they are some of the most expensive undertakings on the planet. Risk follows that long payback term since predicting the pricing structure in an energy market 30 years from now is not able to be precisely done. For example, the nuclear industry claims the reason we scaled back building plants in the 70s was because of public opposition, in fact it was the market price of electricity vs the price of electricity from nuclear that caused a number of bankruptcies. This demonstrated that the nuclear plants under construction and in planning were probably going to experience a similar fate and led to cancellation of about 120 plants.

Today we see the same pattern at work. That first round of nuclear plants rode in on a wave of enthusiasm and concern over energy security**; we were going to have electricity too cheap to meter, nuclear cars in every garage, nuclear airplanes flying nonstop around the world and nuclear rockets taking us to the stars. However, even before Chernobyl or Three Mile Island, the real environmental costs and limitations of nuclear power were starting to overpower the hype in the public mind while simultaneously the industry's economic woes were creating a completely disillusioned policy community.

This round of plants is riding a wave of concern over climate change AND energy security and current US government loan guarantees are a drop in the bucket compared to what will be needed. Since there is no known way to use open markets to finance nuclear plants, these loan guarantees are seen more as a political "last chance" for the industry to prove itself capable of keeping costs down than as actual government support of the industry in the manner that Russia, France, Japan etc practice.

Below is a segment of a Citigroup analysis looking at the prospects of developing "merchant" nuclear power in the UK. It incorporates the renewable and energy efficiency goals already established by government and forecasts the residual market share that would be left for nuclear power to fill.

What the market should not take for granted

GDP impact on demand and load factors

Consensus view is that electricity demand in the wide European region will grow by 1.5% p.a. over the next couple of decades. This is a view shared by UCTE in its latest System Adequacy Report. Although it is virtually impossible to produce irrefutable electricity demand forecast we are tempted to argue that the risks are on the downside since:

1. During the boom years of 2003-07, when GDP growth was strong and infrastructure investment high on the back of very liquid debt markets and due to the convergence of the new EU joiners, electricity consumption grew by 2.1% p.a.

2. Energy efficiency is likely to become a bigger driver as technology advances and as awareness rises. It is important to highlight that such measures also fall under the Climate Change agenda of governments, which has been one of the driving forces behind the renaissance of new nuclear.

As a result, we would expect electricity demand growth to be in the 0-1% range for at least the next 5 years, before returning to more normal pace of 1.5-2%. We therefore see scope for an extra 346TWh of electricity that needs to be covered by 2020 vs. 2008 levels.

Should EU countries go half way towards meeting their renewables target of 20% by 2020 that would be an extra ca. 440TWh. Even if EU went only half way, which by all means is a very conservative estimate, that would still be ca.220TWh of additional generation. Under its conservative scenario A forecast, UCTE expects 28GW of net new fossil fuel capacity to be constructed by 2020. On an average load factor of 45% for those plants thats an extra 110TWh.

Therefore under very conservative assumptions on renewables, we can reliably expect an extra 330TWh of electricity to be generated by 2020, leaving a shortfall of 16TWh to be made up by either energy efficiency or new nuclear.

There are currently 10GW of nuclear capacity under construction/development, including the UK proposed plants that should be on operation by 2020. If we assume that energy efficiency will not contribute, that would imply a load factor for the plants of 18%. Looking at the entire available nuclear fleet that would imply a load factor of just 76%. We do believe though that steps towards energy efficiency will also be taken, thus the impact on load factors could be larger.

Under a scenario of the renewables target being fully delivered then the load factor for nuclear would fall to 56%.

(Bold in original)

Citigroup Global Markets European Nuclear Generation 2 December 2008

As I'm sure you've seen, nuclear power supporters claim that even though nuclear power has very high capital costs, that is ok since they generate so much electricity. Their payoff numbers are based on selling 90%+ of the potential power a plant might generate over its lifetime, however, that is predicated on the assumption that there will be a market for the electricity at a price that will pay off those capital costs. What the Citigroup (and similar) analyses show us is that this hypothetically-perfect-for-them market probably will not exist. The plants will either not sell all of the power they generate (not likely) or they will have to sell power based on the price of fuel only and will have to go through bankruptcy to wipe out/restructure their capital cost obligations.

In 2003 the CBO did an analysis of Bush's $18B 50% loan guarantee program and concluded that:

CBO considers the risk of default on such a loan guarantee to be very highwell above 50 percent. The key factor accounting for this risk is that we expect that the plant would be uneconomic to operate because of its high construction costs, relative to other electricity generation sources."

The only way the projects can be really guaranteed for private investment is if the risk is either shifted to:

1) taxpayers in the form of direct and indirect subsidies and loan guarantees, or

2) to the ratepayers where utilities enter into contracts that guarantee the purchase of the total output of the plant at a set price that is determined not by markets, but by whatever it might cost to build and operate the plant.

**It is important to recall that a primary cause of WWII was energy security and that policymakers knew we were involved in resource wars even then.

Recommended reading:

http://www.olino.org/us/articles/2009/11/26/the-economics-of-nuclear-reactors-renaissance-or-relapse