:hi:

http://www.democraticunderground.com/discuss/duboard.php?az=show_topic&forum=389&topic_id=4221547AIG-FP was founded as a partnership between Hank Greenberg of AIG fame and Howard B. Sosin who was also a trader at Drexel

Joseph Cassano, Mike Milken's protege

Think the $400+K party was bad, check out this guy:

Former AIG Exec at Center of Meltdown Got Paid Millions for Little Work

by Paul Kiel, ProPublica - October 10, 2008 5:35 pm EDT

Tags: AIG, Joseph Cassano, Wall Street Bailout

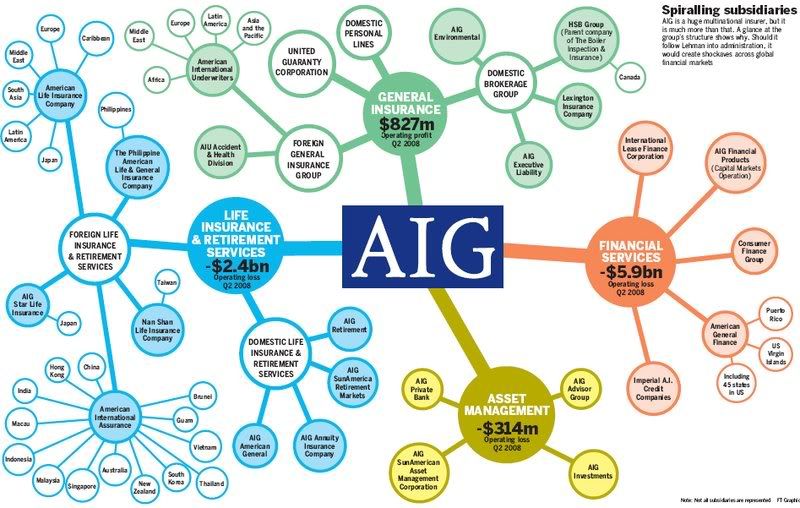

AIG building on Fenchurch Street, London (Clive Gee/PA Wire)One of the biggest reasons for AIG's near failure -- a collapse halted by a government bailout of $120 billion and growing -- was the ballooning losses of a tiny subsidiary called AIG Financial Products. The unit was run by one Joseph Cassano, who resigned in February after his unit, which dealt in credit default swaps, posted $11 billion in losses. (The New York Times says February is also when AIG auditors "identified problems in the firm's swaps accounting.")

But when Cassano left, AIG gave him a sweet deal. Not only was he allowed to keep up to $34 million in unvested bonuses, but the company hired him as a consultant at the staggering fee of $1 million per month.

...

Ashooh couldn't provide an exact date for when Cassano stopped providing services, but said it was the early part of the summer. In other words, even after the U.S. government stepped in to save AIG last month, the man at the center of the company's problems, Cassano, remained on as a million-dollar-a-month do-nothing consultant.

The contract was for a nine-month period to end this coming December. But Cassano and AIG mutually terminated their agreement on Monday, the day before the hearing. The reason, Cassano's lawyer told the Wall Street Journal, was that Cassano's "services were no longer being used."

http://www.propublica.org/article/former-aig-exec-at-center-of-meltdown-got-paid-millions-for-little-work-101 ---------

AIG Replaces Sullivan With Willumstad After Shareholder Outcry

June 16 (Bloomberg) -- American International Group Inc., the world's biggest insurer, ousted Chief Executive Officer Martin Sullivan after record losses, a sagging stock price and criticism from the man he succeeded in 2005, Maurice ``Hank'' Greenberg.

...

AIG's financial-products unit issues credit-default swaps, contracts that promise to reimburse investors for losses on securities that included subprime assets. The business started issuing swaps a decade ago under Greenberg.

Those guarantees declined in value by about $20 billion in the past two quarters. The financial products business was co- founded in 1987 by Joseph Cassano, a former executive at Drexel Burnham Lambert, the securities firm that helped popularize ``junk-bond'' investing before it collapsed. Cassano stepped down in February.

http://www.bloomberg.com/apps/news?pid=20601103&refer=us&sid=atr9TumqGJQo -------

AIG Former Auditor Warned About Derivative Valuation in 2007

By Ari Levy

Oct. 11 (Bloomberg) -- A former American International Group Inc. auditor told the insurer in 2007 that methods used by its financial products division to value derivatives might be flawed, according to documents from a Congressional hearing.

AIG hired Joseph St. Denis to audit the company's accounting, according to testimony at an Oct. 7 hearing of the House of Representatives Committee on Oversight and Government Reform. St. Denis's written statement said he raised concern that certain credit-default swaps might be poised for losses, which wasn't supposed to be possible, and that financial products head Joseph Cassano blocked his input.

``I have deliberately excluded you from the valuation because I was concerned that you would pollute the process,'' Cassano allegedly told St. Denis, according to his written testimony and Committee Chairman Henry Waxman. In September 2007, St. Denis resigned in protest, according to his testimony and Waxman.

....

http://www.bloomberg.com/apps/news?pid=newsarchive&sid=abA6LSQ.3KPM ------

The Reckoning

Behind Insurers Crisis, Blind Eye to a Web of Risk

By GRETCHEN MORGENSON

Published: September 27, 2008

It is hard for us, without being flippant, to even see a scenario within any kind of realm of reason that would see us losing one dollar in any of those transactions.

Joseph J. Cassano, a former A.I.G. executive, August 2007

...

Although Americas housing collapse is often cited as having caused the crisis, the system was vulnerable because of intricate financial contracts known as credit derivatives, which insure debt holders against default. They are fashioned privately and beyond the ken of regulators sometimes even beyond the understanding of executives peddling them.

Originally intended to diminish risk and spread prosperity, these inventions instead magnified the impact of bad mortgages like the ones that felled Bear Stearns and Lehman and now threaten the entire economy.

In the case of A.I.G., the virus exploded from a freewheeling little 377-person unit in London, and flourished in a climate of opulent pay, lax oversight and blind faith in financial risk models. It nearly decimated one of the worlds most admired companies, a seemingly sturdy insurer with a trillion-dollar balance sheet, 116,000 employees and operations in 130 countries.

...

The London Office

The insurance giants London unit was known as A.I.G. Financial Products, or A.I.G.F.P. It was run with almost complete autonomy, and with an iron hand, by Joseph J. Cassano, according to current and former A.I.G. employees.

A onetime executive with Drexel Burnham Lambert the investment bank made famous in the 1980s by the junk bond king Michael R. Milken, who later pleaded guilty to six felony charges Mr. Cassano helped start the London unit in 1987.

The unit became profitable enough that analysts considered Mr. Cassano a dark horse candidate to succeed Maurice R. Greenberg, the longtime chief executive who shaped A.I.G. in his own image until he was ousted amid an accounting scandal three years ago.

But last February, Mr. Cassano resigned after the London unit began bleeding money and auditors raised questions about how the unit valued its holdings. By Sept. 15, the units troubles forced a major downgrade in A.I.G.s debt rating, requiring the company to post roughly $15 billion in additional collateral which then prompted the federal rescue.

Mr. Cassano, 53, lives in a handsome, three-story town house in the Knightsbridge neighborhood of London, just around the corner from Harrods department store on a quiet square with a private garden.

....

http://www.nytimes.com/2008/09/28/business/28melt.html?pagewanted=1&ref=todayspaper (lots more there, good read on how AIG with the help of Cassano's junk bond Milken techniques turned onto mortgages ruined the economy. I know I've seen this here on DU before, but it really is right out of the mob playbook. They took an entity with the best credit there was, the company insuring everything else pretty much, and used it to back this entire market of junk mortgages that everyone (well everyone who had a clue, Krugman for example been saying this for years) knew would blow up one day. There was nothing backing it, just like the scene in Goodfellas where they are selling everything out the back door of a bar the mob has taken over, at a loss. Cassano probably bailed on Drexel just before hammer came down on Milken and the company itself became a felon--still hitting some google).

Drexel?

AIG-FP was founded as a partnership between Hank Greenberg of AIG fame and Howard B. Sosin who was also a trader at Drexel

Cassano was a protégé of A.I.G-Financial Products' first leader, Howard B. Sosin. Both men joined the insurance company from joined A.I.G. from Drexel Burnham Lambert, the Wall Street firm that grew into a junk bond powerhouse thanks to Michael Milken. Drexel collapsed in 1990.

Three years earlier, A.I.G.-Financial products was created as a joint venture between Greenberg and Howard B. Sosin., a former trader from Drexel.

Known as the "Dr. Strangelove of Derivatives," Sosin was regarded as a quantitative genius. He wrote scholarly articles on derivatives and briefly taught at Columbia Business School. Indeed, his inventive wizardry extends beyond the world of finance. He has registered numerous patents, one for a golf club that accomodates a golfer's special swinging style.

In his new job at AIG-Financial Products, Sosin he was given an unusual deal: a 20 percent stake in the unit, and 20 percent of its profits.

Under Sosin, the unit dived deeply into the nascent world of derivatives. It later branched out into energy, currencies, and commodities, and bought assets from cattle to the London City Airport.

But the fast-dealing culture caught Greenberg's wary eye. By the early 1990s, Greenberg, who ruled the company with an iron fist, had grown so concerned about the unit's derivatives dealings that he formed a secret "shadow team" of traders to mimic A.I.G,-Financial Product's trades, according to a former company executive.

(...)

The C.E.O. ordered Sosin to dial it back, but Sosin refused. He left the company in mid-1993 and sued A.I.G. He later received a payout of over $180 million from A.I.G.

(...)

http://www.bnet.com/2459-14037_23-237553.html So Hank Greenberg's story that he trust his successors make sense, because he didn't trust that London unit. So with Greenberg out of the way, Sosin's protege finally had his hands free...

However the name Drexel is familiar:

Early years of J.P. Morgan

Morgan entered banking in 1857 at his father's London branch, moving to New York City the next year where he worked at the banking house of Duncan, Sherman & Company, the American representatives of George Peabody & Company. From 1860 to 1864, as J. Pierpont Morgan & Company, he acted as agent in New York for his father's firm. By 186472, he was a member of the firm of Dabney, Morgan & Company; in 1871, he partnered with the Drexels of Philadelphia to form the New York firm of Drexel, Morgan & Company.

During the American Civil War, Morgan was approached to finance the purchase of antiquated rifles being sold by the army for $3.50 each. Morgan's partner re-machined them and sold the rifles back to the army for $22 each. The military knew it was buying back its own guns, so the so-called 'scandal' turned out to be more about government inefficiency than any chicanery by Morgan (who never even saw the guns and acted only as a lender). Morgan himself, like many wealthy persons, including future Democratic president Grover Cleveland, avoided military service by paying $300 for a substitute.<1>

After the 1893 death of Anthony Drexel, the firm was rechristened J. P. Morgan & Company in 1895

(...)

http://en.wikipedia.org/wiki/J._P._Morgan So what event involved London and J.P. Morgan as well? Wasn't that the Great Depression of 1929 ...