Money and Banking-Part 8: The Private Banking Business

Posted on March 12, 2016 by Eric Tymoigne

By Eric Tymoigne

The US financial system is extremely complicated and this series shades light only on some corners of that system by focusing on the banking sector. Here is a broad picture of the US financial system (some things have changed since the time I made this). Since the beginning of this M&B series, posts have emphasized the importance of balance sheet to get a solid understanding the mechanics at play in the financial sector. This post continues that trend.

The balance sheet of a bank

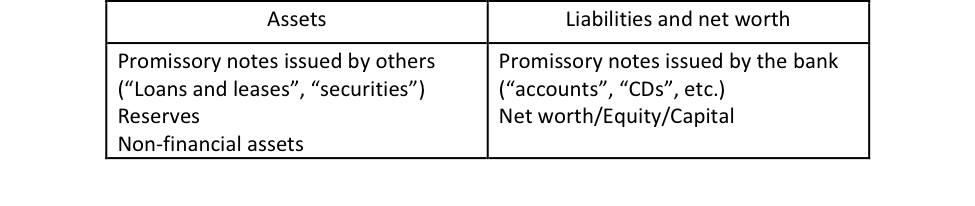

The balance sheet of a private commercial bank looks like this:

Promissory notes issued by others include any kind of agreement between the bank and an entity that made a promise to pay a monetary amount. That entity can be a domestic or foreign, household (mortgage note or any other customer notes), company (business credit, corporate securities), or government (treasuries, municipals). Promissory notes may or may not have a market in which they can be traded. If they have a market they are called “securities”, if they don’t they are called “loans and leases” (I explained in a previous post, and will do it again in the next post, the word “loan” is really inappropriate). A previous post studied in details reserves, which are themselves a promissory note as we will see later, but are singled out for analytical purpose. Non-financial assets include real estate, computers, goodwill etc.

in full:http://neweconomicperspectives.org/2016/03/money-banking-part-8-private-banking-business.html